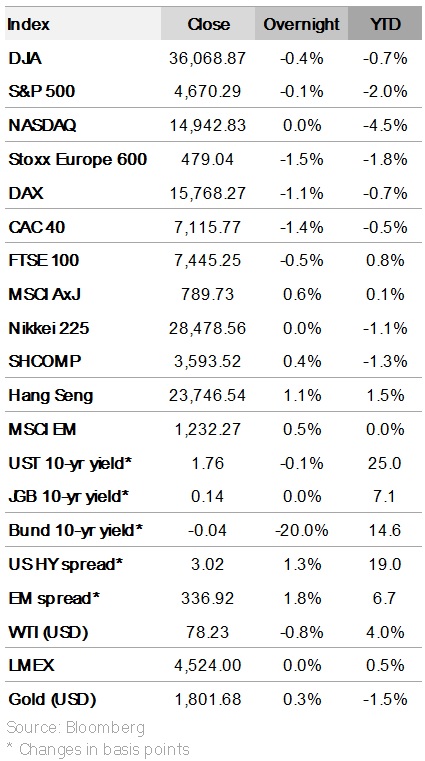

Key Points

-

FX: Rising bond yields drove selloff in commodity and European currencies as investors sought safety in JPY and the greenback

-

Rates: Accelerated taper, rate hikes, and potential quantitative tightening driving USD rates higher

FX: Wary of animal spirits

Monday (10 January) was a telling session regarding fears of an aggressive Fed tightening to rein in US inflation. The US 10Y Treasury yield hit a high of 1.806% before ending the session lower at 1.748%. The 10Y UST yield is still significantly above its end-2021 level of 1.51%. Commodity and European currencies bore the brunt of the selloff and investors sought safety in JPY and the greenback. All said, DXY and EUR are still consolidating in the same ranges seen over the past month. The same can be said for many exchange rates too.

According to prepared remarks for his confirmation hearing today, Federal Reserve Chair Jerome Powell will tell the Senate Banking Committee that the Fed would “prevent higher inflation from becoming entrenched”. Powell’s remarks come ahead of what may be the highest Consumer Price Index (CPI) reading since the early 1980s tomorrow. Consensus expects CPI inflation to rise to 7.0% y/y in December from 6.8% in November. With asset purchases set to end in spring (March to May), a few Fed officials reckoned rate hikes could start early at the Federal Open Market Committee (FOMC) meeting in March. Some private sector forecasters discounted four hikes this year (more than the three signalled at the FOMC meeting in December) and reckoned the Fed might even start shrinking its balance sheet (quantitative tightening) this year.

On Thursday, Lael Brainard will also weigh in on the debate during her confirmation hearing as Fed vice chair. Brainard is considered more dovish and is likely to be more measured in her comments. We remain wary that markets might have gotten ahead of itself over their Fed tightening expectations to the point of believing that the Fed has lost control of inflation. Looking back, the Fed started quantitative tightening in 2018 after five hikes from 2015 to 2017. All said, the S&P 500 did rebound from its 100-day moving average yesterday. So did the Nasdaq Composite after it shed more than 10% from its late November peak. With the Fed believing the US economy is strong enough to pull back its pandemic stimulus, it is difficult to see the Fed agreeing with markets that its actions will result in recession at this early stage.

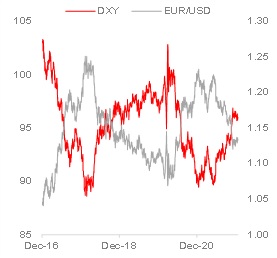

Figure 1: Contrasting fortunes

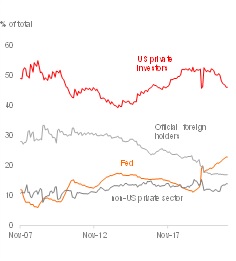

Rates: How to think about QT?

Accelerated taper, rate hikes, and possibly quantitative tightening (QT) – policies that reduce the Federal Reserve’s balance sheet – have brought USD rates sharply higher since the start of the year. While taper and rate hikes are well understood, the impact from QT is less clear. There is some consternation among investors that there could be significant market impact. In the previous cycle, QT was done by setting a cap on the runoff pace. Initially, this was set at USD10b per month in 2017 (when the Fed funds rate was above 1%) and was gradually increased to a peak of USD50b per month in 2019. In this cycle, with the Fed’s balance sheet much more bloated at USD8.8t, there appears to be more urgency to bring the size down. Building policy space (both on the rates and balance sheet fronts) might well be a key consideration. The Fed could kick QT off in the middle of the year, shortly after the rate hike cycle begins.

The impact on the market should be split into two components – the liquidity impact and the duration impact. First, we do not think that the liquidity impact would be significant for many quarters. The Fed’s reverse repo facility is the last resort for excess funds to be parked. If we assume that the Fed runs down the balance sheet at a pace of USD100b per month, it would still take over a year before this facility gets drained. Note that even if that happens, there are still excess reserves in the system. Moreover, a standing facility has also been put in place to add liquidity. In short, a repeat of excess tightness experienced in 2019 (leading to repo market issues) is unlikely to be seen.

The impact on duration is negative, all else equal, but there is a time component. If the Fed reinvests its holdings to keep the balance sheet constant, the Fed still buys assets every month, lending support to US Treasuries (UST). However, if holdings are allowed to mature, this reinvestment stops/slows depending on the cap that the Fed sets. For example, there are chunky maturities months with the largest at USD166b in February. Clearly, there will be some smoothing needed, with the Fed likely to set the run-off rate cap at about USD80-100b. A simpler way to think about it would be to see Fed holdings of UST running down from the current 22% of total outstanding at a faster pace than if the balance sheet was kept constant. As reference, at the start of 2020, the Fed held less than 14% of UST outstanding. That said, the Fed is only one factor impacting rates. We should also consider the improving US fiscal position, likely reduced fiscal stimulus from Biden’s social spending plan, economic conditions, and how the other major players in the market would react. In short, some term premium has to be factored in as a price insensitive buyer of UST fades.

Figure 2: Holders of US Treasuries

GLOBAL CROSS ASSETS

Returns of cross assets around the world