Key Points

- Better growth outlook for ASEAN, but plenty of macro headwinds. Brighter spots in Singapore, Indonesia, and Vietnam

Equities: ASEAN's cautious reopening

Emerging ASEAN remains one of the last regions to reopen as vaccination rates fell behind. We look for a gradual improvement in growth as vaccination rates rise and social restrictions ease in tandem. Following a disappointing year in 2021, the region is set to recover to its pre-pandemic level in 2022, driven by private consumption growth. Some setbacks in manufacturing growth due to Covid lockdowns in 2021 did not derail the robust export outlook for the region, as the region remained a key electronics manufacturing hub. It is alluded that Covid lockdowns in Malaysia, Thailand, and Vietnam contributed significantly to global supply chain disruption.

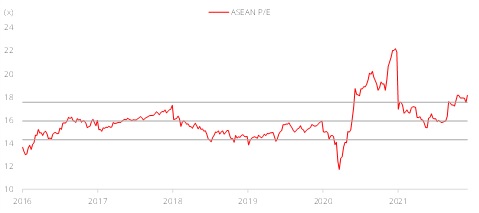

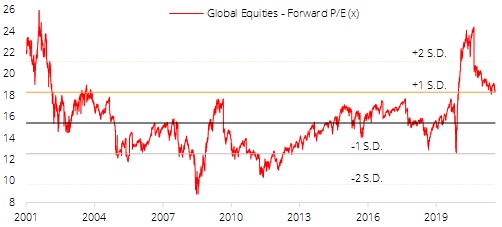

Price-to-earnings (P/E) ratios in ASEAN markets are, however, loftier than pre-Covid, on the back of weaker than expected earnings from lacklustre economic growth. Without valuation tailwinds, we expect ASEAN markets to trade cautiously as they face the risks of the Fed’s QE taper, rising interest rates, the omicron variant, China slowdown, supply chain disruptions, and inflation. The brighter spots are in Singapore, Indonesia, and Vietnam.

Singapore’s “living with Covid” opening took a setback when the new virus strain, omicron, was found. Looking at past periods when tightening measures were implemented, the benchmark Straits Times Index had hovered above 3,000 levels. Vaccination rates are today higher; thus we believe the market would find strong support. Banks and REITs remain attractive at current levels.

An improving Covid situation and a commodity super-cycle is prepping for Indonesia to outperform again in 2022. Coupled with an improving Current Account balance from strong commodity exports and lower imports, the rupiah has held steady as a result. Liquidity remains abundant and will enable credit demand growth next year as the economy reopens.

Progress in vaccination rates towards near 90% in main cities has helped Vietnam make a comeback as the workforce returned to operate factories in Ho Chi Minh and Hanoi’s industrial hubs. Investments and other economic activities are likely to pick up next year. The government is likely to ready a meaningful fiscal stimulus package for 2022/3 as such support measures have been less robust in the past.

Figure 1: No tailwind from loftier valuation

GLOBAL CROSS ASSETS

Returns of cross assets around the world

CIO Markets Watch

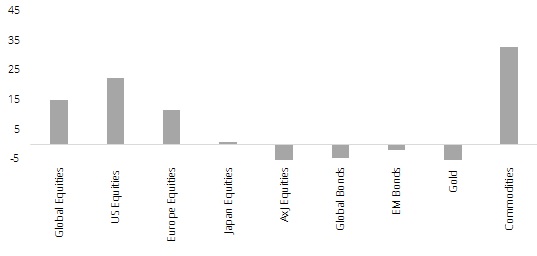

Global Cross Assets YTD Returns

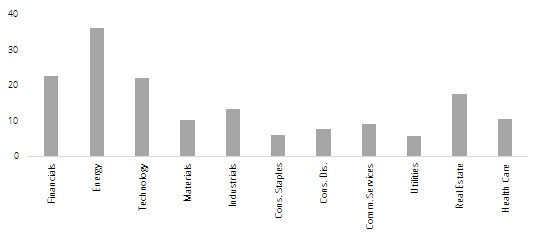

Global Sector YTD Returns

Global Equity Valuation

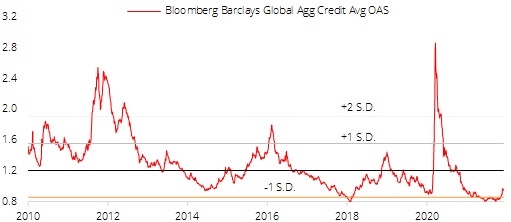

US Corporate Spreads

INDEX RETURNS

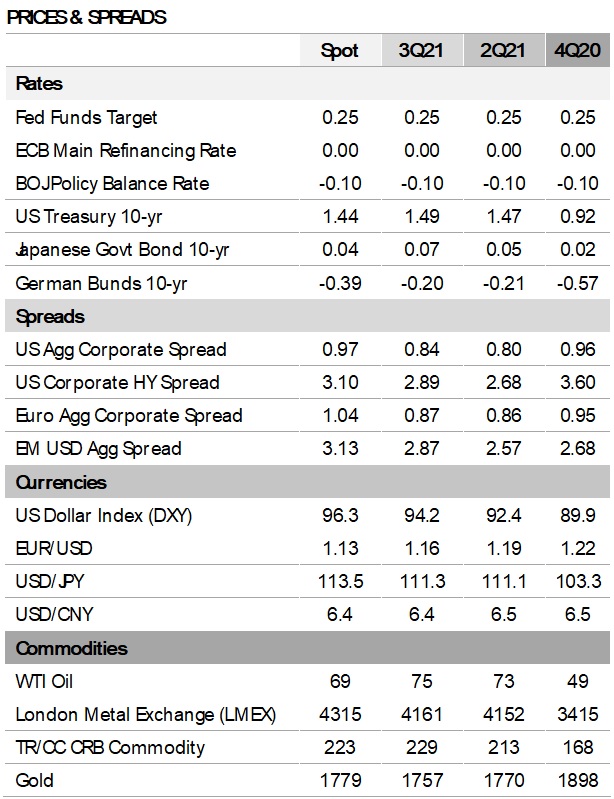

PRICES & SPREADS

CIO Economics Watch

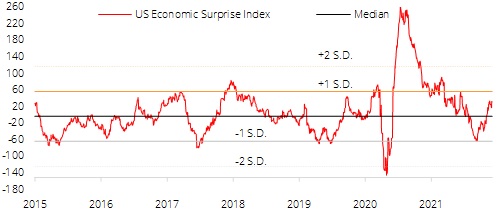

US Economic Surprise Index

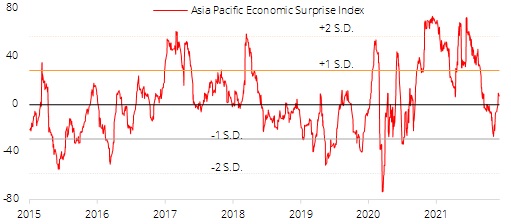

Asia Pacific Economic Surprise Index

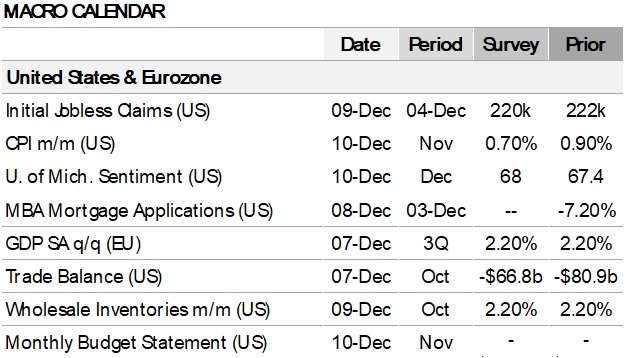

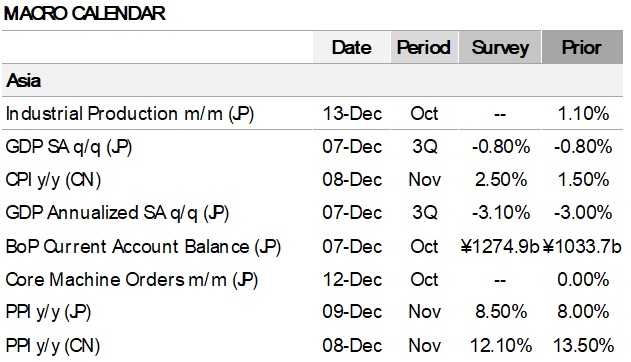

MACRO CALENDAR