Key Points Equities: S&P 500 attractive on a 12-month perspective; Sell-down in Technology reaching a tail-end

Rates: US recession potentially a massive headwind for Asia bonds as investors grapple with dollar strength and widening of risk and term premiums

Equities : Positive 12-month view for S&P 500US corporate earnings remain resilient despite rising rhetoric on recession. US equities have suffered an acute selloff since the start of the year amid rising bond yields and geopolitical uncertainties. Adding on to the proverbial wall of worries are rising recession concerns as elevated inflationary pressure weighs on the outlook for investments and domestic consumption. Indeed, US domestic consumers are essentially stuck between a rock and a hard place today given falling assets prices and rising cost of living.

Despite the domestic headwinds, the earnings outlook for US companies remains resilient. According to Bloomberg consensus, corporate earnings growth (based on calendar year) is still expected at 17.8% in 2022 and 9.1% in 2023. While such a growth trajectory is not what one would typically consider as "spectacular", however, they are also not as dire as what the prevailing rhetoric on recession is suggesting.

The resilience of US corporate profitability can be attributed to two factors: a) Globally diversified nature of US companies’ revenue base and 2) Strong market positioning and ability of US companies in protecting their profit margins.

S&P 500 attractive on a 12-month perspective; Focus on Quality Plays. We have previously analysed how the S&P 500 tends to trade in subsequent 12-months after an acute correction at the start of the year. Our research concludes that US equities have historically rallied 20% on average, with positive returns occurring on four out of five occasions. Such findings underpin our view that the risk-reward of gaining exposure to the US market is looking increasingly attractive. We advise investors to focus on Quality Plays - companies that possess strong pricing power and market positioning.

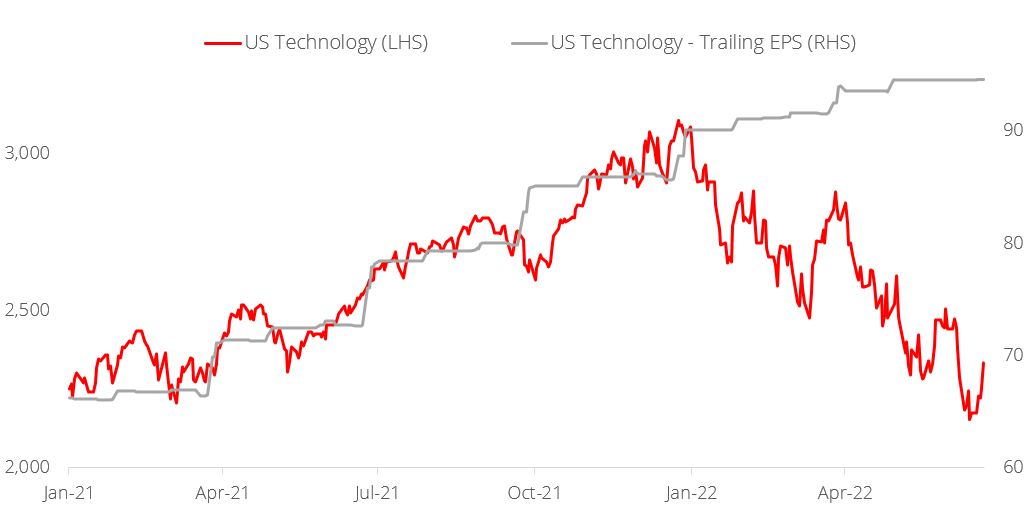

Selldown in Technology reaching a tail-end. From a sectoral perspective, we do not advocate switching out of Technology as we believe the selldown (as a result of rising bond yields) is reaching a tail-end. At the end of the day, the Technology space is backed by resilient earnings and rising bond yields have limited impact on their long-term fundamentals.

Figure 1: US Technology earnings stay resilient