Key Points

-

Equities: US earnings downgrades amid rising recession fear as elevated bond yields weigh on economic activities; Stick to quality plays.

-

Rates: Expect another 75 bps hike at upcoming FOMC meeting; Too early for Fed to downshift its rhetoric.

Equities: US earnings downgrades amid rising recession fear

Recession risks on the rise as elevated bond yields weigh on economic activities. US recession risk is on the rise as surging inflationary pressure and rising bond yields weigh on interest rate-sensitive parts of the economy like housing and investments. The spread between the US Treasury 10Y and 2Y bond yields has undergone inversion and historically, this suggests an impending recession. Similarly, the Bloomberg Economics Probability of US Recession index is also assigning a 37.5% chance of a recession within the next 12 months and 100% within the next 24 months.

Impact of rising recessionary concerns on US sectoral earnings forecast. The prevalence of rising recessionary concerns has prompted earnings downgrades amongst analysts and listed below are our key findings:

-

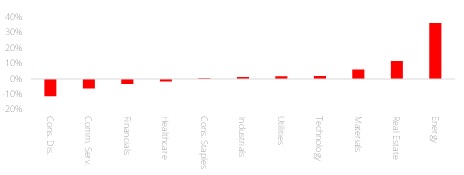

Since end-March this year, the sectors which garnered the largest downward earnings revision are Consumer Discretionary (-11.2%), Communications Services (-6.1%), and Financials (-3.2%). On a trailing 12-months basis, Financials and Consumer Discretionary have registered operating margin contraction of 1.49 %pts and 0.06 %pts respectively.

-

On the flipside, sectors that managed to register the largest upward earnings revision are Energy (+36.2%), Real Estate (+11.6%), and Materials (+6.2%). On a trailing 12-months basis, Real estate and Materials have registered operating margin expansion of 1.25 %pts and 0.25 %pts respectively.

Stick to quality plays. As macro momentum in the US moderates, we advocate investors to stick to quality plays in the S&P 500 and this refers to companies that possess the following traits: (a) Strong pricing power and market positioning, and (b) Has historically demonstrated the ability to outperform during periods of volatility. Given the sharp pullback in US Technology stocks since the start of the year on rising yields concerns, we believe that the prevailing weakness offers a window of opportunity for long-term investors.

Figure 1: US earnings revision since end-March

Rates: Neutral and then…?

We expect another 75 bps in policy rates hike at the conclusion of Wednesday’s (27 July) Federal Open Market Committee meeting, taking the Fed funds rate upper bound to 2.50% (the peak of the previous cycle) and arguably into neutral territory. After that, there will be a tussle between data (which indicate that inflationary pressures are acute) and forward-looking indicators (including easing supply chain issues, lower commodity prices, and lower break-evens) which suggest that price pressures are peaking. While employment indicators still look healthy, the turn in jobless claims as well as the declines in Purchasing Managers’ Indices in the US and the Eurozone bear close watching.

It is probably too early for the Fed to downshift its rhetoric. Declines in transport costs and commodity prices might take some time to feed into broader prices. Moreover, inputted rent might stay elevated for some time. In any case, we do not think that data weakness is sufficient to prompt serious worries from the Fed just yet. Instead, the Fed will probably slow the pace of tightening if data permits as policy settings would already be in restrictive. However, any emphasis on rates being already at neutral and/or indications that downside risks to the economy have surfaced might prompt another round of re-pricing in the market. There may be an asymmetrical reaction to a perceived dovish pivot that may benefit the belly of the curve (5Y tenor).

We prefer to fade extreme levels in pricing. Much like we thought there would be value to go long govvies when 10Y US yields are above 3%, there might be interest to pay rates if 10Y yields fall to 2.70%. Our core view is that the Fed will tolerate a soft-landing to contain inflation, but not engineer a hard landing to replace the inflation problem.

Figure 2: Pulling back