Key Points

-

Equities: Rising rates on the back of broad-based economic recovery will not derail S&P 500.

-

FX: Investors sought safety in the greenback and JPY amid market volatility; Risk aversion hurts commodity currencies most.

-

Rates: Outside change of Fed turning incrementally hawkish at this week’s FOMC meeting.

Equities: Fed monetary tightening and its impact on S&P 500

Fed monetary tightening on the cards amid persistent high energy prices and supply chain disruptions. US inflation is seeing no signs of abating as both headline and “core” US inflation surged 7% and 5.5%, respectively, in December last year. The “stickiness” of US inflationary pressure can broadly be attributed to two key factors:

-

Surging energy prices: Brent crude oil price has rallied sharply to hit USD87.89/bbl (as of 21 January). Weak capex spending among global oil companies will underpin further upside for oil prices with Brent expected to reach USD92.00/bbl by 4Q23.

-

Lingering supply chain pressure: Data compiled by the Federal Reserve Bank of New York suggest that supply chain pressure remains elevated globally.

Persistent inflationary pressure, coupled with the latest Fed narrative on monetary policies, are expected to translate to impending rate hikes this year. We expect the Fed Funds rate to hit 1.00% and 1.75% by end-2022 and 2023 respectively.

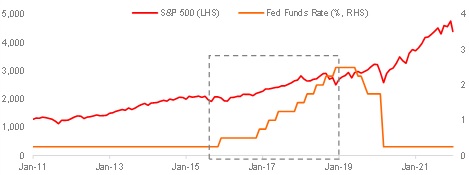

Rising rates on the back of broad-based economic recovery will not derail S&P 500. The rally in the S&P 500 persisted during the previous Fed tightening cycle and this time shall be no different. Beyond the current bout of market volatility as investors grapple with the implications of Fed policy tightening, we expect US equities to resume its uptrend, driven predominantly by resilient corporate earnings.

Based on consensus forecast, S&P 500 earnings is expected to grow 20.3% in 2022, underpinned by EBITDA margin expansion of 1.8 %pts to 22.3%.

Focus on quality plays on S&P 500. As bonds yields grind higher in the coming months, investors are advised to shift to income generative quality plays - companies with strong earnings momentum and market positioning. Quality plays have displayed resilience in the current bout of market volatility and a strong case in point is the US Technology space. "Big Tech" has vastly outperformed the "Emerging Tech" space and we expect this divergence to persist.

Figure 1: The previous Fed policy tightening cycle has no major detrimental impact on S&P 500

FX: Nervous ahead of FOMC meeting

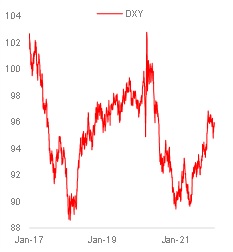

Apart from bonds, investors sought safety in the greenback and JPY amid the persistent selloff in US equities. DXY ended at 95.642 last Friday (21 January) and recovered this year’s losses. After hitting a five-year high of 116.16 on 4 January, USD/JPY fell to 113.68 last Friday. The next support levels for USD/JPY are 113.20 (100-day moving average) and 112.50 (the low in early December). Risk aversion hurts commodity currencies most. NZD and AUD depreciated 1.6% year-to-date and 1.1%, respectively. Having failed to appreciate below 1.25 per USD since 13 January, CAD declined 0.6% to 1.2581 last Friday.

Selling pressure on the American stock market

|

Index |

Dow Jones |

S&P 500 |

Nasdaq |

|

21 Jan close |

34,625 |

4,398 |

13,769 |

|

% YTD |

-5.7% |

-7.7% |

-12.0% |

|

Vs record high |

-6.9% |

-8.3% |

-14.3% |

|

Lowest since |

1 Dec 2021 |

13 Oct 2021 |

3 Jun 2021 |

|

Vs 100d MA |

-3.2% |

-3.9% |

-9.7% |

|

Vs 200d MA |

-2.0% |

-0.7% |

-6.6% |

|

14d RSI |

28.2 |

26.9 |

25.5 |

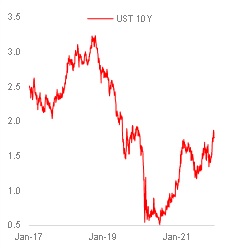

All eyes are on the FOMC meeting on 26 January. The question on everyone’s mind is whether Fed Chair Jerome Powell can stabilise oversold US equities and pave the ground to end asset purchases and increase interest rates in March. During their confirmation hearings a fortnight ago, Powell and Vice-Chair Lael Brainard, told the Senate Banking Committee that the Fed is committed to reining in inflation from multi-decades high to sustain the US recovery and avoid disrupting financial markets. However, US stock markets have reeled from “triple Fed tightening” fears. Last week’s selloff finally sent the US Treasury 10Y yield from its two-year high of 1.874% to 1.758%, flattening the yield curve (10Y vs 2Y spread) to 75.5 bps, near the 73 bps low on 28 December.

Debate rages over what fuelled inflation. One camp blamed the Fed’s ultra-loose policies and Biden’s stimulus packages. The other camp cited supply constraints and labour shortages amid a strong recovery in demand. However, worries unite that persistent and elevated inflation might hurt growth prospects. On 25 January, consensus expects the US Conference Board’s consumer confidence index to slow to 111.8 in January from 115.8 in December. The Atlanta Fed GDPNow model no longer estimates US gross domestic product growth high at an annualised 9.7% q/q saar in 4Q21. On 27 January, consensus sees growth increasing to 5.3% from 2.3% in 3Q21. On 28 January, US Personal Consumption Expenditures (PCE) deflator should rise to 5.8% in December from 5.7% in November, and the core PCE deflator (Fed’s preferred inflation gauge) to 4.8% from 4.7%.

Meanwhile, USD/CAD is supported at 1.25 – the 200-day moving average (dma) – and capped at 1.2630 (100-dma) into the Bank of Canada (BOC) meeting on 26 January. According to a Reuters poll, a slim majority of economists expect the BOC to defer its first hike to 2Q22. However, markets see more than an 80% chance for the BOC to lift its overnight lending rate from 0.25%. According to the BOC 4Q21 Business Outlook Survey, a majority of Canada Inc expect inflation to hold above 3% over the next two years (two-thirds of respondents) from intensifying labour shortages (75%) and higher wages (80%). Hence, USD/CAD is likely to take its cue from whether the Fed can calm markets and whether the BOC or the Fed will hike before the other. The S&P/TSE Composite Index ended last week below its 100-dma. Sentiment will sour if it takes out the 200-dma too.

Figure 2: Risk aversion

Rates: FOMC preview

We see an outside chance that the Fed would turn incrementally hawkish at this week’s Federal Open Market Committee (FOMC) meeting (outcome due 27 January, 3am SGT). Fundamentally, we think that the Federal Reserve is behind the curve and would like to normalise policy as communicated. The 7% Consumer Price Index print for December only worsened matters as inflation has been running faster than the Fed is able to pivot. While omicron has caused jobless claims to spike, we see this as temporary and probably will not detract from the fact that the unemployment rate is already close to 4%. Accordingly, the Fed may end quantitative easing in January (instead of March as previously communicated), providing the clearest signal yet that rate hikes are imminent (we see the first hike in March).

We think that the Fed might go for more optionality and would probably not pushback against current market pricing of about seven hikes over the coming two years. Even as geopolitical risks surrounding Ukraine are mounting, we think inflation is still the biggest risk on the Fed’s radar. Without pre-committing, the Fed could simply signal that every meeting (eight FOMC meetings a year) is live and that there is no pre-set path. This could break the current market assumption that the Fed would proceed at a run rate of one hike per quarter. Signalling a 50 bps to kick off tightening may be too aggressive in our opinion.

With geopolitical risks, weak stock market sentiment and keeping in mind where USD rates are trading at, market movements are likely to be much more nuanced. The market already pricing in four hikes in 2022 and just about three hikes in 2023, it is difficult to argue that the market is unprepared for tightening over the medium term (two years). Further out, risk aversion has also pulled 10Y UST yields back to 1.77%, from a recent peak of 1.90%. USD rates strategy should be split into the different segments as the drivers differ.

There could be opportunities in the front (6M, 9M tenors) of the curve in case the Fed decides to frontload tightening. The run rate for the Fed is likely to be one hike a quarter if things go well. We also think that the Fed will be able to deliver three hikes over the first three quarters of the year. However, there is a non-negligible chance that the Fed will continue inching hawkish (which it has been doing since mid-2021). Should this occur, the early part of the hike cycle when inflation is still high and short rates low would probably be the more likely period where tightening gets accelerated.

The impact on longer-term rates (5Y onwards) would be mixed. Sentiment, which is already dicey, might take a further hit, driving long rates lower initially. Subsequently, once the market has adjusted, we would expect longer-term yields to head higher. We think that 10Y yields close to 1.70% may be an interesting pay opportunity and we think spreading across the 3Y and 5Y makes sense as well. Lastly, we are neutral 2Y UST with the market already factoring in about seven hikes through end-2023, with risks balanced either way.

Figure 3: Hawkish