Key Points

-

Equities: Fed quantitative easing contributing to yield curve distortion; Go for quality plays on S&P 500 as uncertainties mount.

-

Rates: Longer-term USD rates (10Y yields are above 2.8%) pricing in neutral rate after sharp selloff since start of the year.

Equities: Go for quality plays in S&P 500

Fed quantitative easing and yield curve distortion. Recent inversion of the US Treasury 10Y-2Y yield curve (a situation where short-term yields are higher than long-term yields) has sounded the alarm bells on whether this heralds an imminent recession. Since the 1970s, yield curve inversions are historically followed by economic recessions and investors are assuming that this time will be no different.

But as we have argued in our report CIO Perspectives - Don't fear the curve inversion (dated 1 April 2022), prolonged periods of Federal Reserve quantitative easing may have inadvertently led to distortions in the yield curve, diminishing its usefulness as a predictor of recessions along the way.

Indeed, quantitative easing has the effect of suppressing the term premium (which is the additional yield needed to compensate an investor for taking on additional duration risks). From January 1995 to November 2008, the term premium averaged 1.0%. However, since December 2008, the average term premium has fallen to 0.1%.

Lower term premium weighs on long-term bond yields and our analysis suggests that if a normalised term premium is used instead, the yield curve will currently be at a level that is far from inversion.

Go for quality plays on S&P 500 as uncertainties mount. Global risk assets will continue to face the proverbial wall of worries in the coming months as inflation and geopolitical concerns mount. In such a challenging environment, we advocate investors to go for quality plays in their securities selection. Quality companies with strong branding and market positioning are able to pass on rising costs in an inflationary environment to end consumers and protect their profit margins.

As Figure 1 shows, the 12-month trailing operating margin for US quality companies has exceeded those of the broader market by an average of 3.7 %pts since 2019. The strong buffer in profitability provides the necessary downside protection as input costs grind higher, in particularly across the commodity space. In terms of return on equity (ROE), US quality companies similarly possess higher ROE than the broader market by 8.5 %pts on average.

Figure 1: US quality companies possess strong profit margins

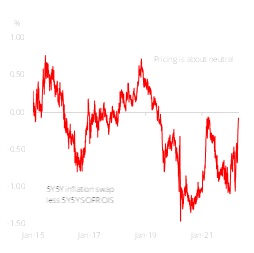

Rates: Longer-term rates are pricing in neutral

After a sharp selloff since the start of the year, longer-term USD rates (10Y yields are above 2.8%) are finally pricing in neutral. We would again emphasise that neutral is relative to where inflation expectations are. We think 5Y5Y real rates might be the best way to sidestep supply side pressures arising from economic reopening and the Russia-Ukraine conflict. By capturing the medium-term perspective, it is clear that the Fed on path to normalisation should bring real rates close to zero, something that we had flagged back in January. 5Y5Y real rates are now at 0.07%, up close to a 100bps since the start of the year

Accordingly, we are also neutral on long-term rates, noting that our 2Q forecast of 2.80% has already been hit. There can be considerable swings on either side of 2.80% as market participants grapple with uncertainties over the terminal rate for the cycle and fears about quantitative tightening. This fear is reflected in elevated implied and realised rates volatility. Note that implied rates volatility is the single largest stress point amongst indicators that we track. 2Q would likely mark peak duration fears, in our opinion. As the market prices in a Fed that brings policy settings into restrictive territory, the market may well take longer-term rates higher than neutral as well. However, at these levels, we are reluctant to chase USD rates higher, noting that a large chunk of the move may already be done. We are also not convinced that steepening is a trend that can persist in a Fed tightening cycle and prefer to fade the 2Y/10Y close to 40 bps.

Figure 2: 5Y5Y Implied Real Rates