In the Second Part of the series on Structured Products, we dove deeper into what goes into the building of a Structured Product, including the various underlying assets and derivative contracts like options and swaps. In Part 3, we explain how different Structured Products are designed for different investment goals, and how you can choose your investments based on this information. For the illustration, we have categorized investors into three profiles: Conservative, Balanced, and Aggressive.

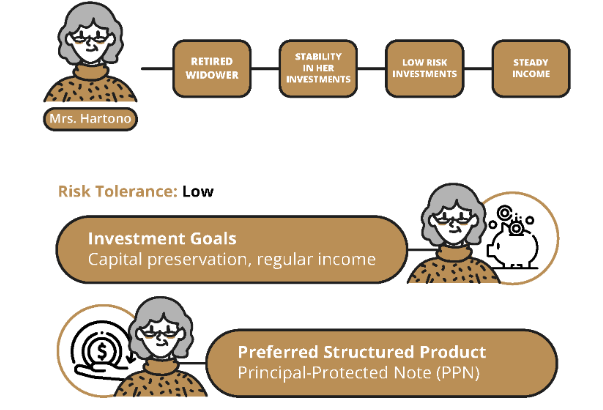

Conservative Let’s call the Conservative investor Mrs. Hartono. She is a retired widower, who has spent her career building up her savings. Therefore, she is averse to risks on her savings, and values stability in her investments. She wants to ensure that her money is protected while generating a steady income in her retirement. Therefore, her profile looks as below:What is a PPN?

A Principal Protected Note guarantees minimum return equal to the principal, even if the underlying assets perform poorly, because of Principal Protection (refer to Article 1 of this series for the definition of Principal Protection). However, to accrue the benefits of a PPN, the investor must hold the notes until maturity, which can tie up funds for a long time.

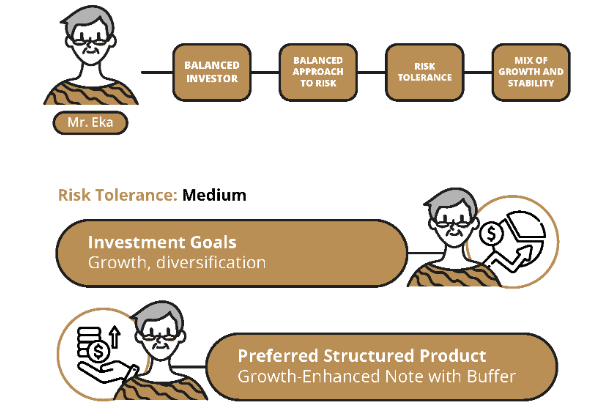

Balanced Let’s call the Balanced investor Mr. Eka. He has a balanced approach to risk, being comfortable with some volatility in his investments, but with potential rewards. He’s looking for a mix of growth and stability. His profile looks as below:

What is a Growth-Enhanced Note? Growth-Enhanced Notes offer the potential for investors to participate in the positive performance of the underlying asset, earning a return linked to the growth of the asset. Te buffer, on the other hand, refers to a range within which the investor’s principal is protected. For example, a 5% buffer will protect the principal if the asset value falls by less than 5% during the investment period. It is important to note, however, that the buffer does not eliminate losses entirely, especially when the asset value drops below the buffer rate.

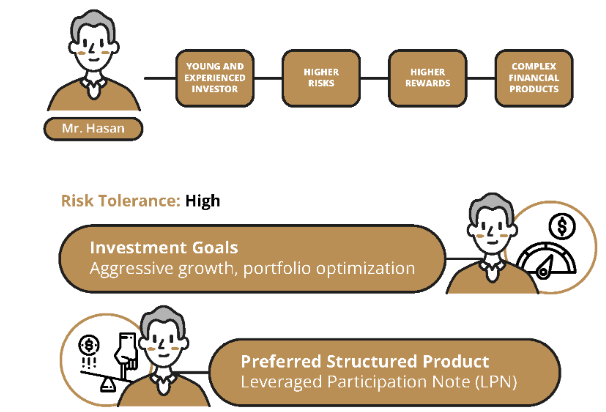

Aggressive Let’s call the Aggressive investor Mr. Hasan. He is a young and experienced investor willing to take on higher risks for potentially higher rewards. He’s actively engaged in the markets and is comfortable with complex financial products. His profile, therefore, looks thus:

What is an LPN? A Leveraged Participation Note uses leverage, determined by Participation Rate, to amplify the returns on an asset. A 2x Participation Rate, for example, will double the returns. These high rewards also have the downside of high risk: if the value of the asset falls, the losses incurred are also determined by the Participation Rate — a 5% drop at 2x Participation Rate can lead to a 10% loss. LPNs are subject to market fluctuations and require intricate knowledge of financial instruments.

The Simple Summary

The specific Structured Product you should invest in depends on your investment goals, the kind of growth you wish for, and the level of risk you are willing to take. Some other Structured Products that can be classified based on which profile they benefit most are:

Conservative — Capital-Protected Notes, Fixed Income Products like bonds

It is recommended, as always, that you set out your investment goals clearly, and do a thorough market research before making any investments. You can get in touch with your investment advisor for more details.

In Part 4 of our series, we will take a closer look at Interest Rate-linked Investments.