Key Points

-

Equities: The secular uptrend in the Technology sector is to persist.

-

Rates: UST curve inverts much easier in periods of stagflation; 1970s' growth pessimism, coupled with Fed hikes, led to deeply inverted curves.

Equities: Technology - Secular uptrend

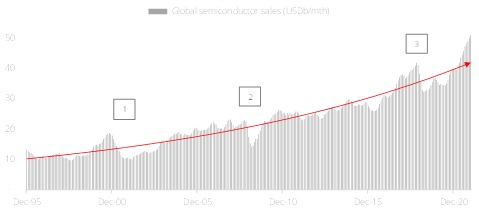

The performance of the Technology sector has been impacted by the Russia-Ukraine conflict. Since the start of the year, technology sector has corrected 14%, despite the fact that revenue of the global semiconductor industry rose 26% to reach a historical high of USD556b in 2021 as chipmakers ramped up production.

The supply-demand balance will remain favourable among leading industry players riding on persistently elevated demand. Notably, the promising demand situation is expected to continue the uptrend in 2022 driven by the emergence of new innovations and as countries scramble to build up upstream technology capability.

Global semiconductor monthly sales have been in consistent uptrends, spearheaded by continuous integrated circuit development, node migration, increased in embedded functionality, capacity expansion, and surging adoption of chipsets in electronic devices.

Since 1995, there were only three occasions where the sector’s growth momentum was interrupted (Figure 1):

-

Dot-com bubble

-

Global Financial Crisis

-

Covid pandemic

These corrections occurred in 2000, 2008, and 2020, which were not at all related to any geopolitical tensions. Subsequent to each of these black swan-driven events, the growth momentum of technology sales recovered strongly within a short period of time, justifying the sturdiness of the sector as end demand has been primarily driven by relentless innovations and technology advancement.

Going forward, the sector’s growth trajectory will remain robust spurred by the creation of chipsets with more complicated functions, circuit layout to deliver interconnected processing power, wider range of logic functions, and larger memory storage capacity.

As such, the global upstream technology sits well in the Growth side of the CIO Barbell Strategy.

Figure 1: In leaps and bounds

Rates: Assessing Stagflation & Recession risks

The most direct spill over from the Ukraine-Russia conflict is via the inflation route. With supply chain and sanctions impeding the flow of commodities (wheat, oil, and gas in particular), the inflation picture, already problematic due to Covid, just got worse. Unfortunately, we do not see an easy solution to the inflation issue even if the conflict gets resolved as sanctions will likely still remove a chunk of commodities from the world economy. The upshot to this is that inflation will be higher for longer. This is also reflected with 10Y breakevens touching 2.85%, up from 2.49% in early February. Unfortunately, inflation at persistently high levels could drag on GDP growth. In particular, we would be watching to see if wage growth can keep up to ensure that there is no substantial decline in purchasing power that would undermine the US consumer.

What does it mean for USD rates? Clearly, policymaking will be more complicated but we doubt that the Federal Reserve would be derailed. To be sure, the market has pared expectations of the pace of Fed hikes as growth worries emerge. However, the Fed operates on a dual mandate of full employment and stable prices. With the unemployment rate at 3.8%, half of the mandate has been met. Unless the labour market deteriorates, inflation is still the biggest issue for the Fed. The period from the 1970s is instructive as the Fed raised rates with rising inflation, even if that means that growth takes a hit. Current market pricing is probably more a function of risk aversion driving down term rates, thereby underestimating what the Fed would do in a period of high inflation. While worries on growth have emerged, we reckon that the US (with a strong labour market) is still well placed to handle the storm. Moreover, the global economy does have a post-omicron tailwind going. While the US Treasury (UST) curve has flattened tremendously, risks of a recession are not as elevated as headlines suggest.

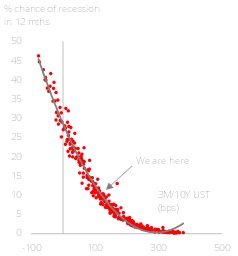

The UST curve (defined as 3M/10Y here) could invert much easier in periods of stagflation. In the 1970s, pessimism on growth, combined with Fed hikes led to deeply inverted curves for years. The current situation has similar echoes with commodities exacerbating already elevated price pressures amidst a lack of confidence that growth will hold up. The curve has also flattened much quicker than in a typical hike cycle. Our base case remains that the Fed will hike seven times through 2023 and that growth worries are probably largely sentiment driven at this point. We remain firmly in the pay on dips camp and would spread pay tenors across 3Y, 5Y, and 10Y rates. Longer-term rates should drift higher once risk aversion fades. If inflation stays in the high single digits and the US economy stalls (our risk case), we will likely see an inverted curve.

Figure 2: US recession probabilities and 3M/10Y UST curve