Key Points

-

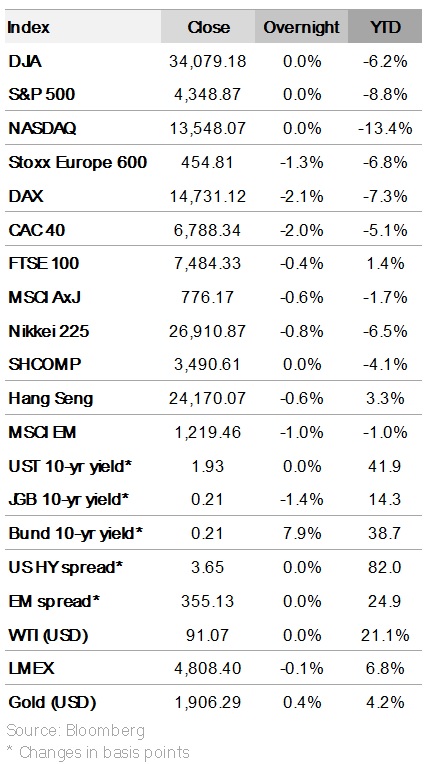

Equities: Equity markets to stay volatile as the Ukrainian crisis escalates.

-

Rates: Modelled neutral for 10Y yields is now hovering around 2.50% amid rising Fed hike expectations.

Equities: Equity markets to stay volatile as Ukrainian crisis escalates

Dramatic escalation in the Ukrainian crisis amid Russia’s recognition of separatist regions. Russia President Vladimir Putin's recognition of two separatist regions, Donetsk and Luhansk People's Republics in eastern Ukraine, has dramatically escalated the Ukrainian crisis. Under decrees signed by Putin, the Russian military has entered these regions on a "peacekeeping" operation, with the troops look set to stay indefinitely. As tension in Ukraine continues to escalate, we look at how this crisis could affect the global economy and financial markets in the coming months.

-

Economic impact: The risk of economic contagion from the Ukrainian crisis is low given that Russia accounts for only 1.8% of global gross domestic product (vs 24.7% for US and 17.4% for China). Similarly, in terms of global trade flows, Russia accounts for only 1.7% of global exports (vs 12.1% for China and 9.5% for US). On the flip side, a bigger threat arising from the crisis will come from surging energy prices.

-

Financial impact: A common assumption among investors is that military conflicts are devastating for financial markets. However, drawing from the experience of major military conflicts since 1990, the data suggest otherwise. On average, global equities rallied 38% during military conflicts. Rising uncertainties, meanwhile, triggered average gains of 138% for gold and 89% gains for crude oil.

What happens if Russia invades Ukraine? Highlighted below are the potential impacts on financial markets should Russia invade Ukraine:

-

Oil prices to surge: In the event of an invasion, oil prices will surge due to supply squeeze. Europe relies on Russia for 40% of its LNG demand through pipelines across Europe, and supply could be disrupted due to sanctions on Russia and political unrest in the region.

-

Gold as an effective geopolitical hedge: An invasion by Russia will translate to further upside to gold prices towards our USD2,000 target. Speculators are building up gold positions to hedge against geopolitical risk where gold has long been considered a shelter for volatility.

-

IG credit and treasury bonds as safe havens: During episodes of uncertainty, global credit - especially Investment Grade (IG) names – can act as a buffer for the unpredictability of outcomes.

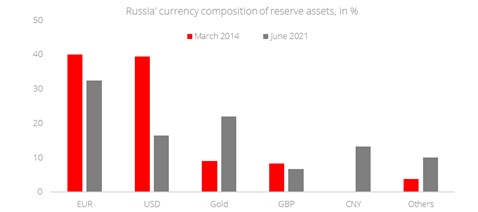

Figure 1: Central banks buy Gold for reserve diversification

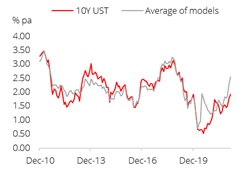

Rates: A relook at our 10Y model amid Ukraine and Fed uncertainties

Considerable worries around the expected Fed and path, as well as elevated Ukraine tensions have led to conflicting forces on US yields over the past few weeks. We relook at our 10Y US Treasury model to get a sense of how rich/cheap yields are at current levels. Our modelled neutral for 10Y yields is now hovering around 2.50%, much higher than where they were at the start of the year. The model suggests that even if we take the recent peak in 10Y yields (at around 2.05%, representing about 55 bps of increase since the start of the year), Treasuries still look significantly overvalued compared to fundamentals.

Much of this can be attributed to rising Fed hike expectations. On this point, the market had been reluctant to factor in the Fed tightening last year. However, recent inflation and employment prints suggest that a much more aggressive stance is needed. In any case, recent Fed speak supported the point that the market had already anticipated. The global component (capturing G-10 growth and interest rates expectations) was the second key factor driving rates higher as central banks take turns to signal normalisation. The other components of that drive rates are mixed. While current inflation fears may be high, Treasury Inflation-Protected Securities (TIPS) are not showing increased worries. Instead, 5Y5Y breakevens are hovering below 2.50%, suggesting confidence that the Fed will be able to get inflation under control. Meanwhile, term premium is probably more compressed than current growth dynamics suggest. Instead, worries about Ukraine (especially in the immediate term) and lingering concerns on Covid variants may still be holding 10Y yields down. We maintain that meaningful dips in USD rates should be paid into.

Figure 2: Actual vs average of models