Key Points

-

Rates: Sharp repricing of USD rates curve after Friday's CPI release; Market sees at least one 75 bps move this year and a terminal Fed funds rate of 4%.

Rates: How Much More to Go?

The repricing across the USD rates curve since Friday's (10 June) Consumer Price Index (CPI) release was one for the ages. The entire US Treasury (UST) curve (2Y and above) is now above 3%, the market now sees at least one 75 bps move for this year (which might get delivered this week, although we still think odds are in favour of 50 bps) and expects a terminal Fed funds rate of 4%. Prior to the CPI beat, the market was content with a few 50 bps moves before a downshift later this year and saw the Fed funds rate peaking in the 3-3.25% region. Having broken the 3.2% top (also a key resistance level) seen in early May, 10Y yields closed at 3.36%, close to our forecast of 3.5%. The upshot is that nobody is keen to hold duration risks into the Federal Open Market Committee (FOMC) meeting where Fed Chair Powell will almost certainly have to sound hawkish.

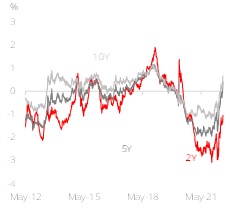

We are watching to see when and where the upshift in USD rates will stabilise. The CPI print and survey-based inflation expectations suggest that the Fed should move. However, with a significant amount of tightening suddenly factored in, there should be a dampening impact on growth and inflation. Much like how stresses in the market in early May marked an interim top in rates, we might be able to get some respite post FOMC meeting. It might not be that easy to beat the hawkish hurdle already set by the market as USTs continue to sell off. We would also note that 10Y implied real yields are now close to 0.68%, in the restrictive zone (which we tag to be in the 0.5-1.0% range) and 10Y breakevens have fallen close to 2.68%, suggesting confidence that the Fed can get a grip on inflation.

We see upside risks to our shorter-term USD rates forecasts, noting that inflation is proving stickier than we had anticipated. While the Fed may not ultimately deliver all the hikes priced, persistent inflation worries are likely to keep rates buoyant for some time. We are also cognizant that growth worries could be revisited later this year. Curve wise, flattening is now taking place at an accelerated pace (quicker than our forecast suggests). We have always subscribed to flattening in the 2Y/10Y and to receive the 2Y/5Y/10Y fly. We think that both strategies have room to play out. Flattish / inverted curves in the 2Y/10Y, 5Y/30Y and 2Y/30Y are very likely in the coming few quarters as the market grapples with a hawkish Fed / growth worries.

Figure 1: UST implied real yields

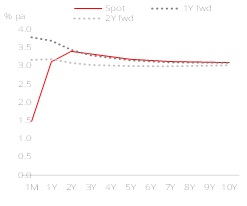

Figure 2: SOFR OIS Curve - Pricing in Fed hikes