Key Points

-

FX: DXY holding its ground between 97.7 and 99.4; EUR under pressure from stagflation worries in Germany.

-

Rates: Robust jobs data sent UST 2Y yield higher; Exceedingly low longer-term yields (10Y and beyond) not warranted.

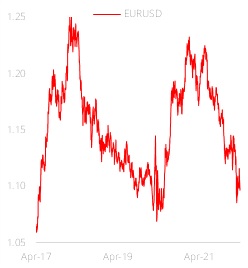

FX: Tough balancing acts

DXY is holding its ground between 97.7 and 99.4. Last week, the US Treasury yield curve (or the 10Y-2Y differential) turned negative for the first time since September 2019. Fed speakers are likely to play down US recession risks following the strong US jobs report last Friday while acknowledging the uncertain economic outlook. They will likely emphasise the Federal Reserve’s objective to return interest rates to more neutral levels of 2% to 2.5% as deliberate and methodical. However, a larger 50 bps hike will be considered at the Federal Open Market Committee meeting on 4 May if the US inflation readings firm again in March.

EUR is under pressure from stagflation worries in Germany. EU bond yields eased last week despite a spike in Germany’s CPI inflation to 7.3% y/y in March from 5.1% in February. Instead, the focus fell on the downgrade in Germany’s 2022 growth forecast to 1.8% from the 4.8% estimated in November by the government’s panel of independent advisers. The GfK consumer confidence index plunged from -8.5 in March to -15.5 in April, its weakest since February 2021. The German government also activated an emergency plan to conserve gas and secure supplies to ease cost-of-living pressures. Germany imports 40% of its gas from Russia which Moscow wants to be paid in roubles. The European Central Bank (ECB) is expected to hold monetary policy steady at next week’s meeting on 14 April. The ECB should keep to its timetable whether to end net asset purchases at the 9 June meeting. Today, a drop in the April’s Sentix Investor Confidence index (-9.4 consensus vs -7.0 previous) could prompt speculators to lighten their gross long EUR positions. If so, EUR could return to the lower half of its 1.08-1.12 trading range of March.

GBP is biased lower towards 1.30 after failing to rise above 1.32. According to CFTC data, speculators accumulated gross short GBP positions on hawkish Fed hike bets. Speculators also reduced their gross long GBP positions on the Bank of England’s hikes turning dovish. Policymakers conceded that high inflation had become a cost-of-living crisis flattening real household income. The Office for Budget Responsibility slashed its 2022 growth forecast to 3.8% from 6%. To add injury to hurt, a post-Brexit drop in UK’s exports to the EU widened the trade deficit to a record GBP16.2b in January vs GBP5.2b in January 2021.

JPY weakness is limited to 125 per USD. The Bank of Japan conducted unlimited bond purchases and defended the 10Y Japanese Government Bond yield at 0.25%, the ceiling under its yield curve control framework. Similarly, USD/JPY peaked 125 on 28 March and retreated to 122.50 on verbal intervention. However, JPY bears continued to buy USD/JPY whenever it dipped below 121.50, believing policymakers would refrain from actual interventions. Still, the fact remains that USD/JPY has not been able to sustain any rise above 125 since mid-2002.

Figure 1: Under pressure

Rates: On track for Jumbo hikes

Market worries about potential economic weakness in the US were unfounded. Last week’s labour market data were firm. Nonfarm payrolls registered 431,000. While this was not as strong as consensus had expected, there was 95,000 in positive net revisions over the past two months. Instead, the focus was on the fact that the unemployment rate fell to 3.6% while average hourly earnings bounced to 5.6% y/y, underscoring how tight the labour market has become. US Treasuries reacted accordingly, sending short-term yields another leg higher as the market gravitates towards jumbo-sized (50 bps) hikes in the coming few meetings.

The impact on longer-term yields was muted, with the 2Y/10Y spread now inverted to the tune of 8 bps. While we do think that flat/inverted curves are inevitable, we are not convinced that longer-term yields (10Y and beyond) should be this low, either in relative or absolute terms. Instead, there still is some lingering pessimism about growth and perhaps some rebalancing flows (supporting bonds) taking place after one of the worst quarters for fixed income in recent decades. There may be some complacency on duration with Fed minutes due on 7 April (2am, SGT). The Fed has communicated that 50 bps hikes are on the table. However, there has been a lack of clarity on how the Fed intends on shrink its balance sheet. If there are hints of a more aggressive rolloff schedule or that the Fed is open to selling securities (especially mortgage-backed securities), duration fears might resurface. We think 10Y yields around 2.30% is a decent pay level.

Figure 2: Inversion