Throughout this series, we have brought to you the definitions of Structured Products, potential returns, associated risks, their derivatives, underlying assets that determine payoffs, and a guide on where to invest based on your investor profile. In this fourth and final part of the series, we will take a closer look at one specific type of Structured Product — Interest Rate Linked Investments (IRLI).

Fixed dan Floating Interest Rate Linked Investment Interest Rate Linked Investment (IRLI) is an investment product in which the performance is linked to reference interest rate movement so that customers have the opportunity to get attractive returns, which are influenced by changes in prevailing interest rates, including both fixed and floating interest rates. They play a crucial role in the financial landscape by offering opportunities for both capital protection and income generation.

The yield in the form of a fixed rate always increases from year to year, and is therefore also know as a Fixed Rate Step Up. Fixed Interest Rate-Linked Investments are suitable for conservative investors looking for minimal risks with stable and predictable income, while protecting their initial investment.

The yield, when in the form of a floating interest rate, can vary according to the reference interest rate, typically a benchmark like LIBOR. Floating Interest

Rate-Linked Investments may be attractive for aggressive investors as they offer the potential for high returns in a rising rate environment. However, there are additional risks involved with floating interests because market rates may fall and lead to losses.

Risk of IRLI IRLI is a form of Structured Product that carries risks not normally associated with ordinary bank deposits. The Customer should therefore not treat IRLI as a substitute for ordinary savings or time deposits. Also, investors can incur losses when they redeem the investment before the maturity date, and because the IRLI is not transferable or negotiable, the bank can deduct any losses that might be incurred from the redemption.

The bank may also choose to redeem the IRLI at the Early Redemption Amount on the Early Redemption Date. In that case, if the investor reinvests the notional Principal Amount, the yield on the reinvested IRLI may be significantly lesser than on the first.

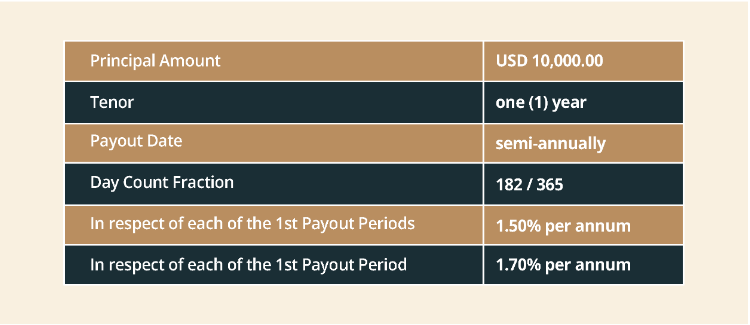

A Simulation To understand the working of IRLI better, let’s consider an illustrative example.1

Assumption The yield is in the form of a fixed interest rate which will increase in respect to each of the payout period (Fixed Rate Step Up).

Scenario 1 (Best Scenario) Payout Amount on Payout Period based on 1st Payout Rate

Principal Amount × Payout Rate × Day Count Fraction USD 10,000.00 × 50% p.a. × 182/365 USD 79 (Gross) = USD 59.82 (Net) Payout Amount on Payout Period based on 2nd Payout Rate

Principal Amount × Payout Rate × Day Count Fraction USD 10,000.00 × 70% p.a. × 182/365 USD 77 (Gross) = USD 67.82 (Net) On Maturity Date, the Customer will receive Principal Amount USD 10,000.00

Scenario 2 (Worst Scenario) If the Customer requests for an early withdrawal of the IRLI in accordance with the early withdrawal requirements and the Bank agrees to the Customer's request, the Customer will receive an early withdrawal amount determined by the Bank. Such early withdrawal amount will usually be substantially less than 100% of the Principal Amount and in the worst-case scenario, such early withdrawal amount is zero. The Customer will not receive any quarterly payout following such early withdrawal.

Benefits of IRLI With the right strategies in place, an IRLI can provide many benefits to investors. These include income generation, especially with the yield that can be in the form of a fixed rate that always increases from year to year (Fixed Rate Step Up) that ensures a steady flow of increasing interest income and potential reinvestment opportunities.

IRLIs can also be integrated into a diversified portfolio to manage overall risk, and provide an additional layer of portfolio protection since they interact differently with other asset classes. Other benefits include 100% Principal Protection if held until Maturity Date, higher returns as compared to traditional deposits, and the potential to continue earning high and fixed yields when the reference rate is in a downward trend.

The Simple Summary Interest Rate-Linked Investments are attractive to both conservative and aggressive investors, providing either a steady income or high returns, depending on how they are customized for different profiles. However, it is important to stay informed about market trends and economic indicators before making crucial decisions. Factors like central bank policy and economic data can influence interest rate movements.

We therefore advise considering Market Outlook and Trends before investing in any IRLI. You can find updates on trends and opportunities on our CIO Insights page. You can also get in touch with your advisor for a detailed walk-through on investing with DBS.