Related Insights

The USD sell-off that began last Friday is gaining traction and momentum. Weak USD sentiment initially channelled through USD/JPY, which continued to grind lower despite unconfirmed reports of Japanese authorities’ intervention and the New York Fed’s monitoring USD/JPY rates. The DXY Index found little support even as markets pared back expectations for more Fed cuts this year.

Record-high gold prices above USD5000/oz point to a structural repricing of geopolitical risk embedded in the USD-centric global financial system. US President Donald Trump’s ambition to assert control over Greenland acted as a catalyst, reinforcing perceptions that US policy is increasingly willing to weaponize trade and finance tools, even against allies. This has eroded the assumption that the USD is a neutral, rules-based reserve asset. Beyond geopolitical neutrality, gold’s appeal also stems from its role as a hedge against rising concerns about fiscal profligacy.

Domestically, political risks are also weighing on the USD. Some Republican lawmakers have begun breaking ranks over Trump’s immigration policies following the Minnesota shootings, alongside growing unease over his efforts to undermine the Fed’s independence. This raises the prospect of Republicans losing control of at least one house at the November midterms, reducing the odds of a repeat of the “Trump Trade” that propelled the USD during the 2024 presidential elections. Trump himself has shown little concern about the USD’s decline, describing it as helpful in addressing his long-standing complaints over perceived undervaluation of the CNY and JPY. His remarks about the USD seeking its own value echo the broader MAGA agenda and references to a potential “Mar-a-Lago Accord,” reminiscent of the 1985 Plaza Accord.

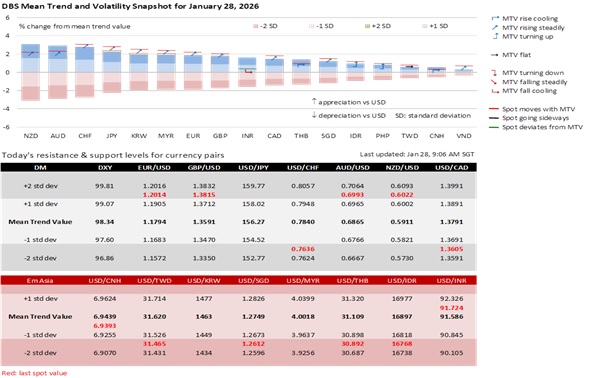

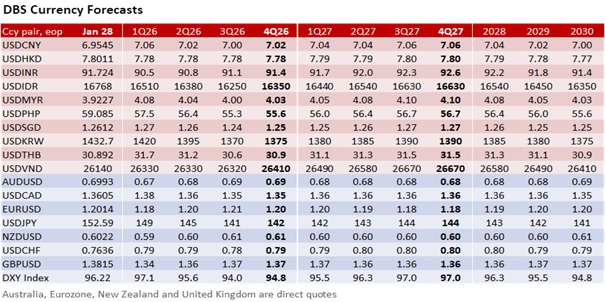

As a result, the USD depreciation we anticipated over the first 6-9 months of this year is materialising earlier and at a faster pace than expected. Several currency pairs have already breached our “weak USD” targets set for 3Q26. USD/CNY and USD/MYR were first to head below 7.00 and 4.00, respectively, followed by GBP/USD above 1.37, AUD/USD above 0.69, USD/CHF below 0.78, and USD/VND below 26320. Other pairs are now approaching our 3Q26 targets, including EUR/USD at 1.21 and USD/THB at 30.6. Additionally, the broad USD weakness is providing some relief to some troubled Asian currencies such as the IDR and PHP. The INR could also benefit marginally from the landmark EU-India trade deal.

What is needed today is whether the DXY can continue to slide after today’s FOMC meeting. Markets will weigh Fed Chair Jerome Powell’s defence of the Fed’s independence against signals that the rate-cutting cycle may be nearing a pause. Trump also said he would soon nominate Powell’s successor, a choice he expects would lower interest rates. The balance here will determine whether the recent USD weakness evolves into a sustained downtrend that prompts a new round of downward revisions to USD forecasts.

Quote of the Day

“We are drowning in information but starved for knowledge.”

John Naisbitt

January 28 in history

The Lego company patented the design of its Lego bricks in 1958.

Topic

Explore more

E & S Macro StrategyGENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.