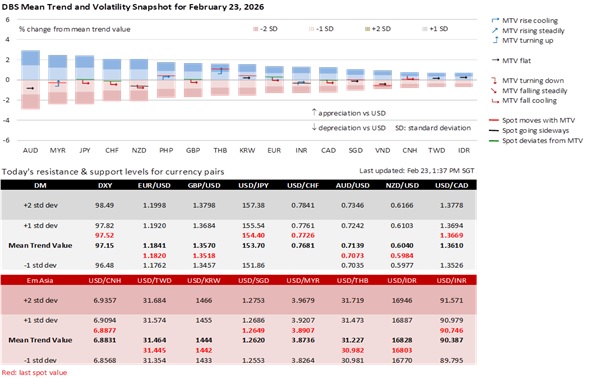

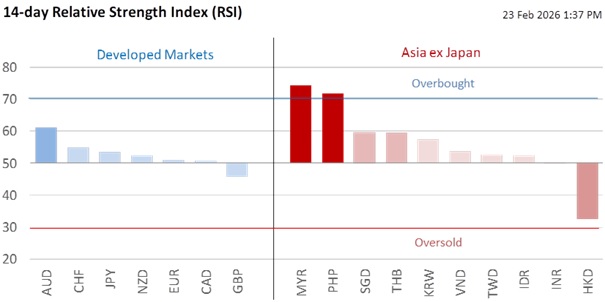

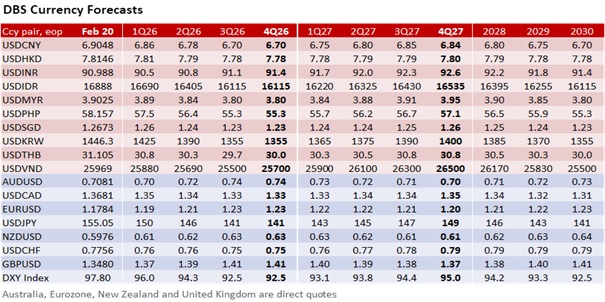

Related Insights

The US Supreme Court ruled 6-3, on February 20, that the International Emergency Economic Powers Act (IEEPA) did not grant President Donald Trump the authority to unilaterally impose Liberal Day tariffs. The tariffs imposed under Section 232 (National Security) for steel and aluminum, and under Section 301 (Unfair Trade Practices) remained in effect.

President Trump’s immediate move to invoke Section 122 to impose the 15% global tariff ceiling indicated no liberation from his broad tariff policies. The “new” tariffs will take effect on February 24, followed later by Trump’s State of the Union (SOTU) address. Trump will likely use this platform to explain his shift to Section 122 and rally support for his trade agenda.

Section 122 subjects Trump’s trade policy to significant procedural complications. These 15% tariffs will expire after 150 days if Congress denies his administration’s request for a formal extension, which will require more permanent Section 301 investigations that span at least 9-12 months, a formal and evidence-based process that cannot be bypassed. Trump could try to restart the clock to bypass the 150-day limit, which the court may view as making law (a power reserved by Congress) rather than executing law. However, the Supreme Court’s ruling has already signaled a willingness to strike down such “transformative expansions” of executive power.

While the Supreme Court’s decision is considered a legal victory for importers, the matter of refunding the IEEPA tariffs has been deferred to the Court of International Trade. Trade experts reckon that administrative processing could take months, even in the best-case scenario, with the protest and litigation path potentially taking years.

Meanwhile, the US exceptionalism narrative has weakened significantly. Advance GDP growth decelerated to an annualized 1.4% QoQ saar in 4Q25, well below the expectations for a slowdown to 2.8% from 4.4% in 3Q25. The trade deficit increased rapidly to USD70.3 bn in December from USD53.0 bn in November and USD28.7 bn in October. The full-year deficit reached USD902 bn in 2025, barely changed from USD904 bn in 2024.

Conclusion: While the Supreme Court’s decision does not remove Trump’s tariffs, it erodes their durability. The Court’s decision to draw a line on Trump’s trade leverage will likely see trade partners leaning towards diplomatic engagement rather than retaliation over tariffs. Trump’s trade agreements signed with many countries under the now-invalidated IEEPA framework may lack a legal basis.

The Supreme Court ruling seeks to reassure markets that the US institutional guardrails remain intact. However, it does not eliminate the policy unpredictability in Trump 2.0. While foreign governments are unlikely to abandon the USD, they will continue to quietly diversify trade channels and marginally reduce USD settlement exposure. They will closely watch the November midterms to determine whether policy volatility will become episodic or structural.

Quote of the Day

"The world of reality has its limits; the world of imagination is boundless.”

Jean-Jacques Rousseau

February 23 in history

The Pulitzer Prize-winning photo of US Marines raising the US flag in Iwo Jima was taken in 1945.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.