Sources:

1 Schroders, “A short history of responsible investing”, published November 28, 2016. Retrieved from https://www.schroders.com/en/insights/global-investor-study/a-short-history-of-responsible-investing-300-0001/

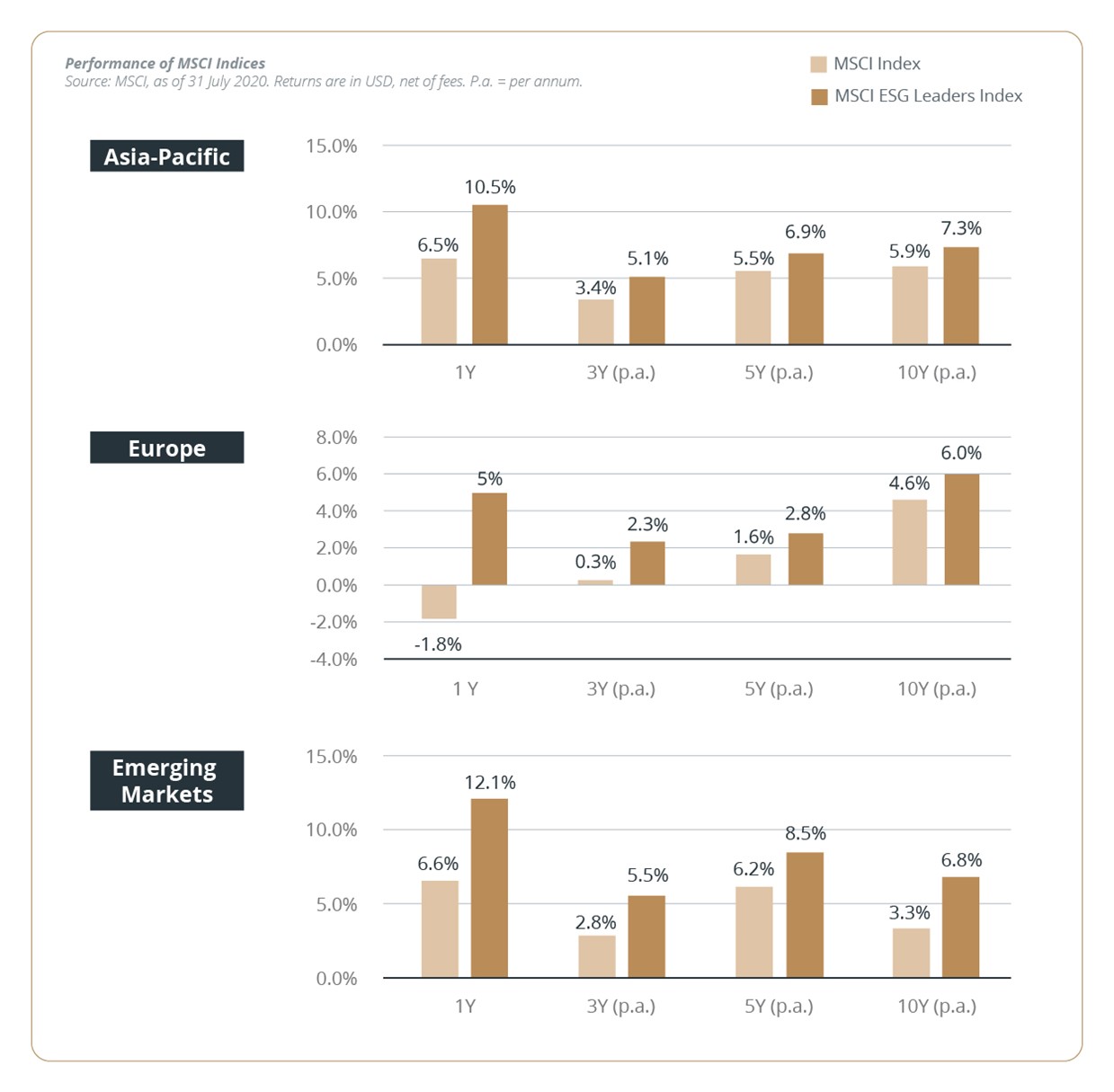

2 MSCI, “ESG 101: What is ESG.” Retrieved from https://www.msci.com/what-is-esg

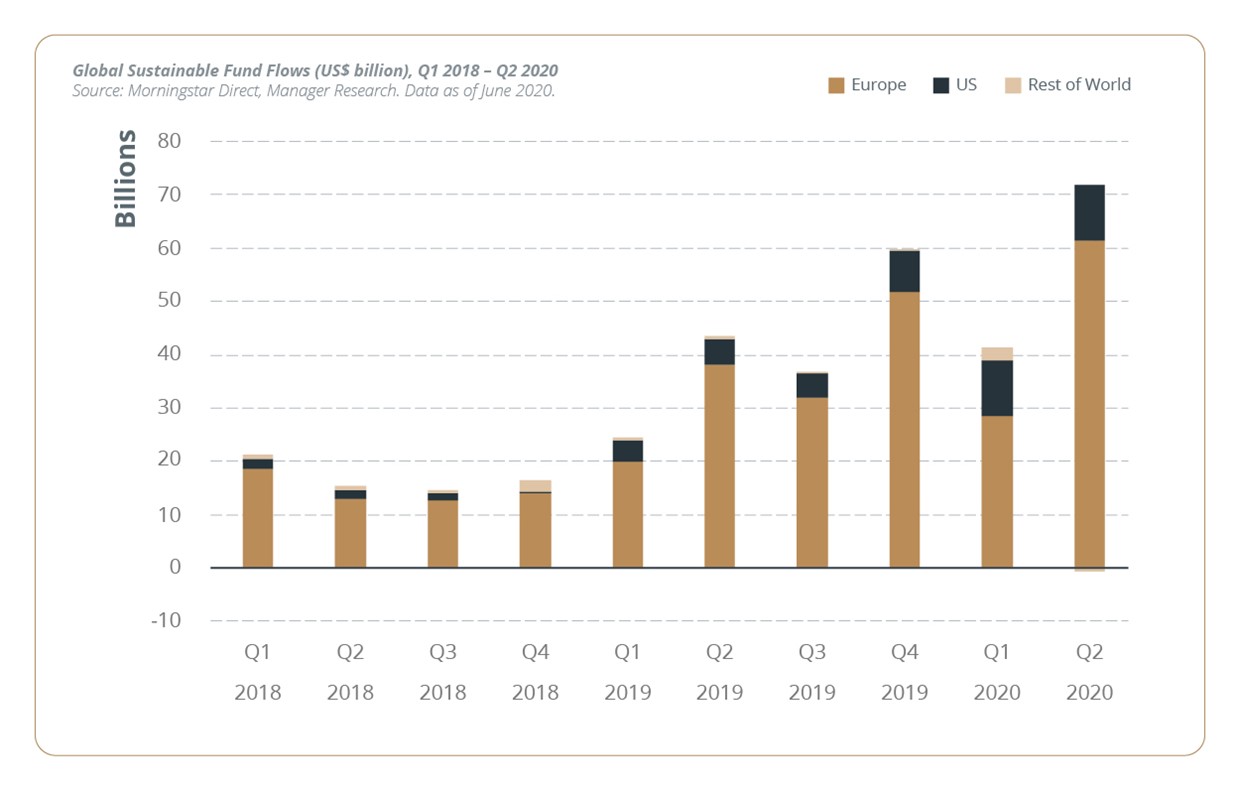

3 Morningstar Manager Research, Global Sustainable Fund Flows report, 2Q20. Retrieved from https://www.morningstar.com/lp/global-esg-flows

4 CFA Institute’s interview with Jeroen Bos, Head of Global Equity Research, ING Investment Management, “How to Integrate ESG Considerations into Investments”. Retrieved from https://blogs.cfainstitute.org/investor/2014/01/20/how-to-integrate-esg-considerations-in-investments/

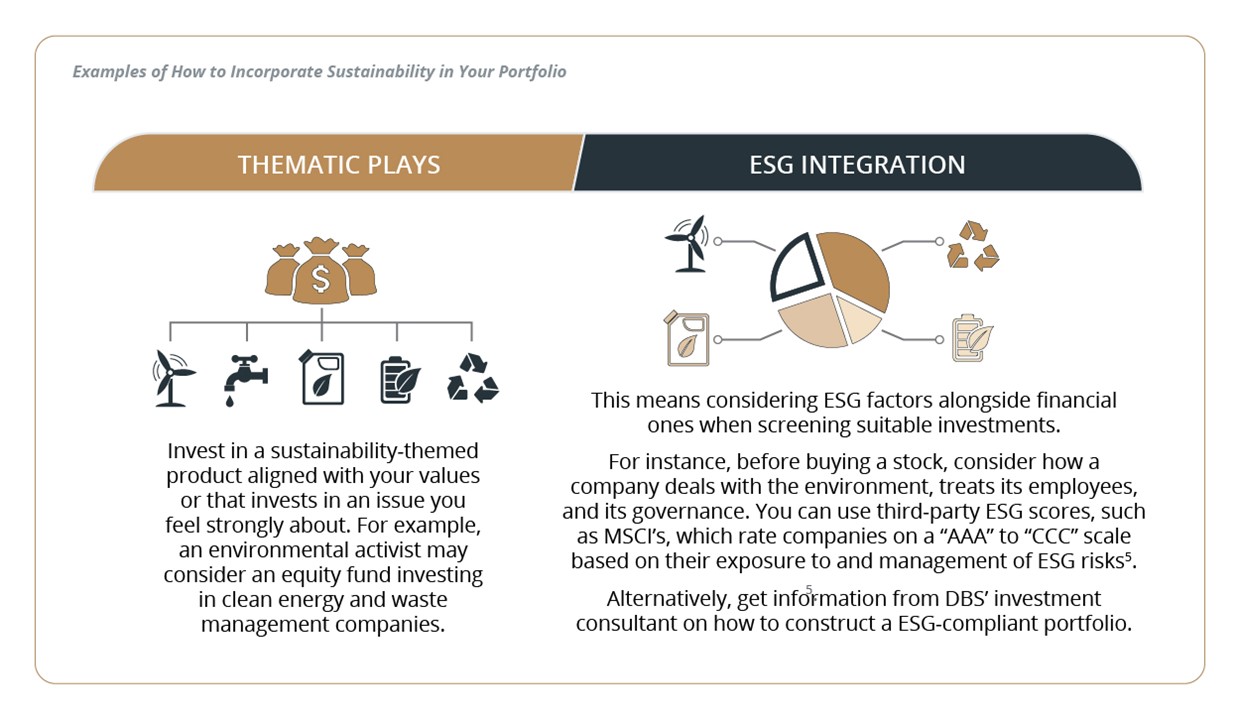

5 MSCI, “ESG Ratings”. Retrieved from https://www.msci.com/esg-ratings

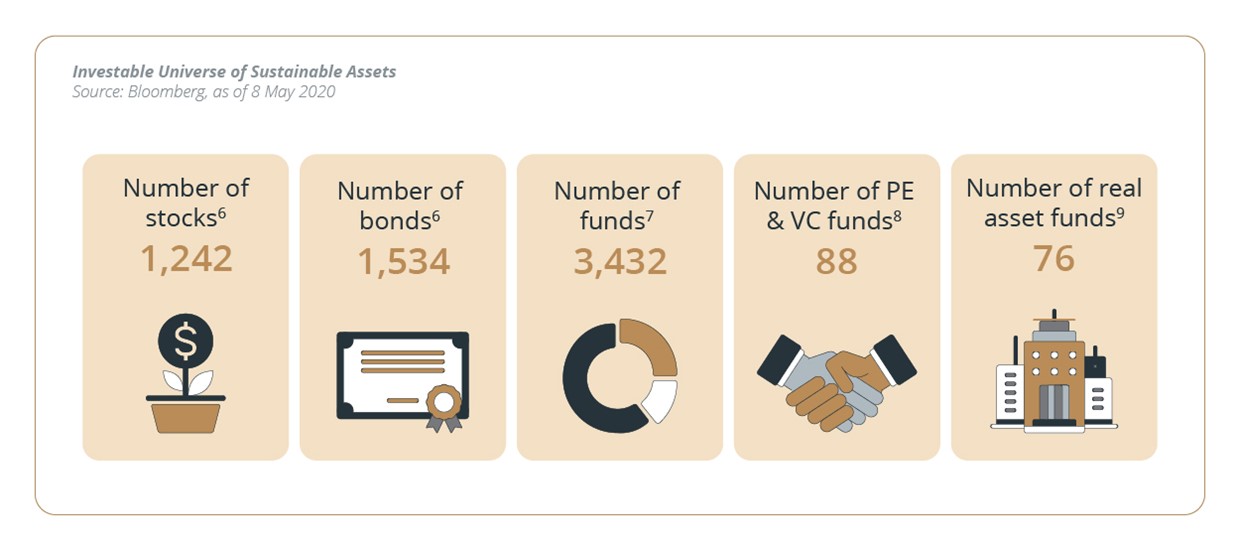

6 Number of constituent equities and bonds in MSCI ACWI ESG Leaders Index and MSCI USD Investment Grade ESG Leaders Corporate Bonds Index, respectively, as of June 2020. Retrieved from https://www.msci.com/msci-esg-leaders-indexes

7 Morningstar Direct, Morningstar Research. Data as of June 2020. Number of open-end funds and exchange-traded funds globally that use ESG criteria as a key part of their security-selection process and/or indicate that they pursue a sustainability related theme and/or seek a measurable positive impact alongside financial return.

8 Cambridge Associates, Private Equity and Venture Capital Impact Investing – Index and Benchmark Statistics. Data as of March 31, 2020. Includes private equity (growth and subordinated capital) and venture capital funds that intend to generate social impact and target risk-adjusted market-rate returns. Retrieved from https://www.cambridgeassociates.com/wp-content/uploads/2020/08/PEVC-Impact-Investing-Benchmark-Statistics-2020-Q1.pdf

9 Cambridge Associates, Real Assets Impact Investing – Index and Benchmark Statistics. Data as of March 31, 2020. Includes timber, real estate, and infrastructure funds that intend to generate social impact and target risk-adjusted market-rate returns. Retrieved from https://www.cambridgeassociates.com/wp-content/uploads/2020/08/Real-Assets-Impact-Investing-Benchmark-Statistics-2020-Q1.pdf

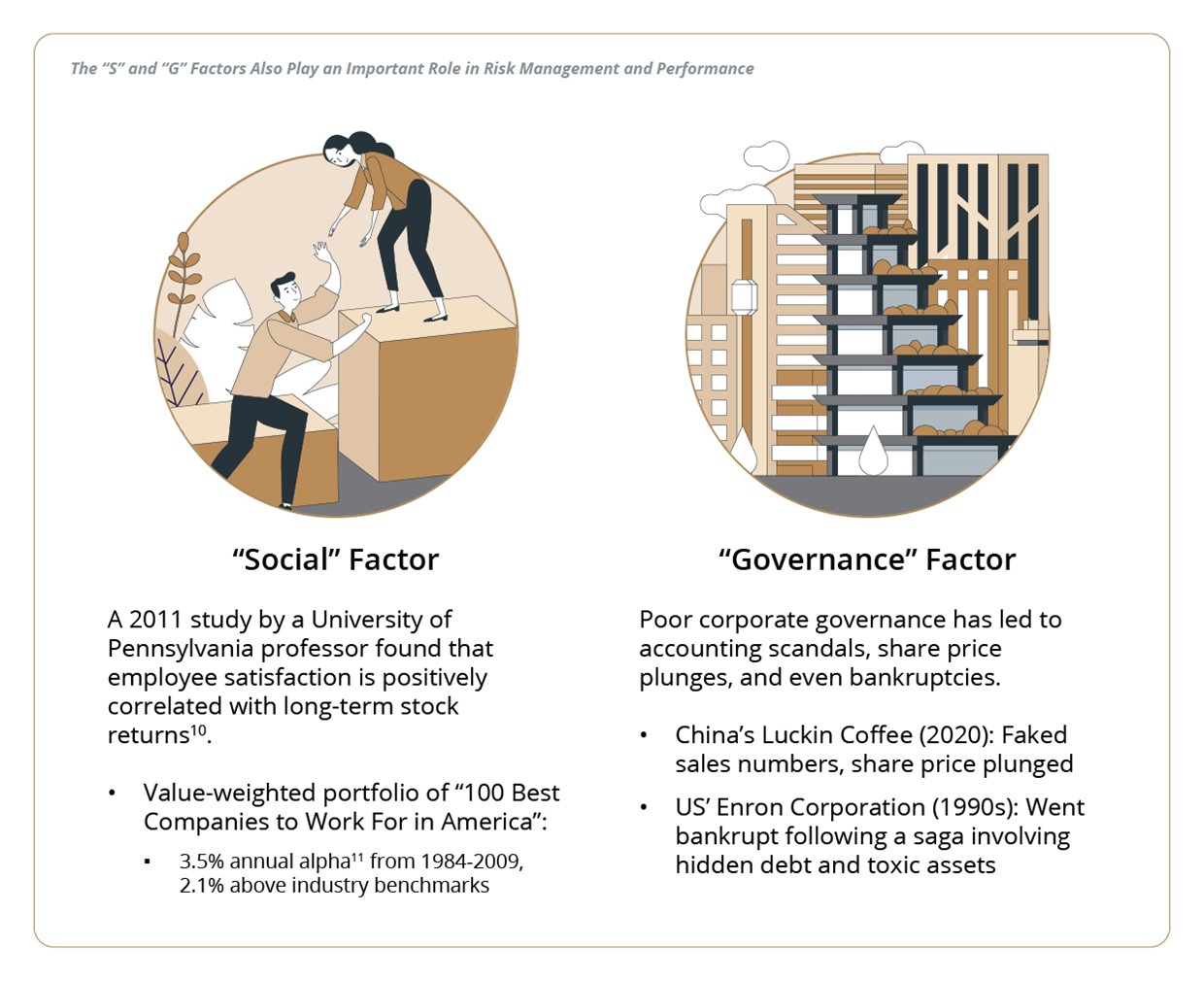

10 Edmans, A. (2011). Does the stock market fully value intangibles? Employee satisfaction and equity prices. Journal of Financial Economics, 621-640. Retrieved from http://faculty.london.edu/aedmans/Rowe.pdf

11 In investment management, alpha refers to an investment’s excess return relative to a benchmark index. The study used the Carhart four-factor model to measure alpha (market, value, size, momentum).

DISCLAIMER

This publication is distributed by PT Bank DBS Indonesia (DBSI). DBSI is licensed and supervised by the Indonesia Financial Services Authority (OJK) and a member of the Indonesia Deposit Insurance Corporation (LPS). This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.