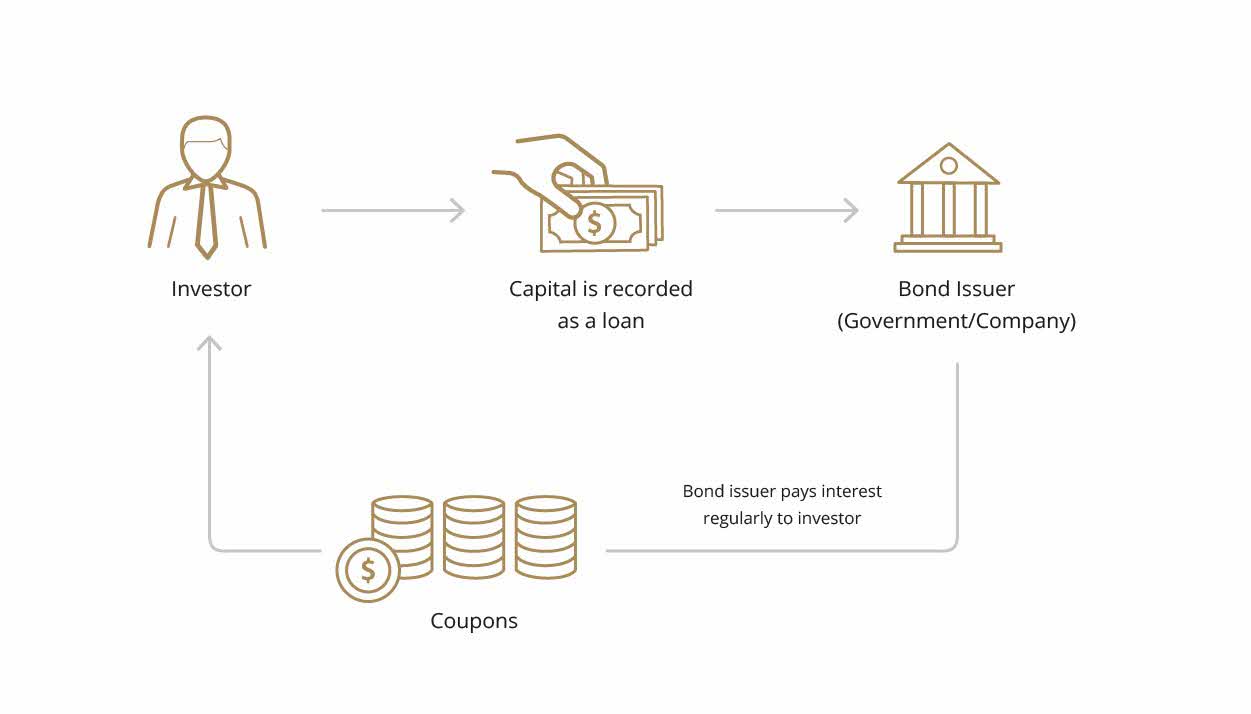

Bonds are debt instruments. That means when you buy a bond, you are lending money to the company or government institution issuing the bond for a fixed rate of return.

Typically, in a traditional bond, there is a coupon, which may be regarded as the interest you are receiving for lending your money. The coupons are paid at fixed intervals, quarterly, semi-annually or annually. As this becomes a source of regular income for the investor, bonds are also known as fixed income products.

Generally, the greater the risk, the higher the amount of coupon you should receive as compensation for lending your capital to a borrower with poorer credit quality. The amount of coupon is also generally higher for longer-dated bonds, which have a longer lending period before maturity.

In the traditional bond, there is a legal obligation on the bond issuer to repay the principal amount invested at the maturity date, which marks the end of the term of the bond.

Understanding Bond Terminology

Par Value

The par value or the face value of a bond is the amount that the bond issuer has borrowed from the investor.

Coupon

The fixed rate of interest to be paid by the bond issuer to the investor multiplied by the par value of the bond.

Coupon 3% x Par Value IDR 1 billion = IDR 30 million annual interest payment

Fixed Income

The amount received in coupons at regular intervals is the investor’s fixed income per year.

Current Yield

Bonds are typically tradeable. As market prices vary from the par value, the current yield of a bond is the annual interest payments of the bond divided by the bond’s current market price.

Callable

This means the issuer can buy back the bonds, paying investors the principal prior to the maturity date.

Step-up

This means the coupon payable rises on a set date.

Benefits of Bonds

Provided the bond issuer is in good financial standing, bond holders get priority to the bond issuer’s cash flow ahead of shareholders and get paid the coupon at regular intervals.

If the bond issuer is in good financial standing, bond holders will be repaid their principal at the maturity of the bond.

Against the uncertainty of the market price of stocks and the dividend earned by those stocks, the promise of fixed income and the eventual repayment of the principal is a stabilizer and a useful diversification tool.

Bonds are lower risk than equities (stocks or shares) to the extent there is a legal obligation for the bond issuer to pay bond holders their regular coupon ahead of any payment of dividends to shareholders.

Risks of Bonds

The risk of the bond issuer being financially unable to pay the promised coupon or repay the principal on maturity.

When investors need to sell their bonds before maturity, there is the risk they may have to accept prices below the par value of the bonds.

Like any market-traded instrument, bond prices fluctuate, depending on the market’s perception of the financial strength of the issuer company, the economic outlook, and the interest rate outlook.

While the fixed income of bonds is an attraction, the risk is being locked into fixed compensation for lending your money even when interest rates are rising.

It may be difficult to find ready buyers for some corporate bonds. Investors needing to urgently sell their bonds may be forced to accept losses if market sentiment is not favorable.

Bonds are a capital market product and the Bank only acts as a Bond Product Selling Agent. Therefore, investment in Bond products is not part of third-party deposits in the Bank so it is not guaranteed by the Bank and is not included in the scope of the government guarantee program or deposit insurance program.

Bank DBS Indonesia as your trusted wealth management partner presents a new era investment on Secondary Bond products for sustainable benefits in managing, growing, and protecting your wealth. Investment on Secondary Bond can be made online through the digibank by DBS Application.

Please allow us to contact you to explain thoroughly by filling your personal data

here .

PT Bank DBS Indonesia is registered and supervised by the Financial Services Authority (OJK) and is a guarantee participant in the Deposit Insurance Corporation (LPS).