Markets will watch US non-farm payrolls tonight, and another weak read will solidify expectations of a Fed rate cut this month. Meanwhile, Stephen Miran, who is currently Chair of the Council of Economic Advisors in the White House, has vowed to uphold the Fed’s independence at his Senate hearing overnight, and could be appointed as a Fed Governor in time for the coming Sep 17 FOMC meeting. Miran has stated in his hearing that there was “no evidence” that Trump’s tariffs were stoking inflation, and his presence in the Fed will reinforce dovish voices in the committee. The USD may slip broadly as markets price in a more dovish-leaning Fed.

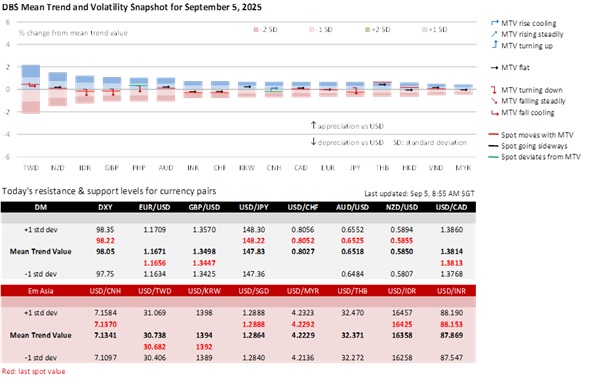

Political risks are also adding to noise in global markets. The French government led by Prime Minister Bayrou faces a confidence vote next Monday, and Bayrou has reportedly not been able to convince the leftwing Socialists or the far right to support his budget plans to narrow the fiscal deficit. French political uncertainty could restrain the EUR, which has consolidated around 1.16-1.17.

In Japan, the LDP will also decide on Monday whether to hold a party leadership election to replace PM Ishiba. Given LDP’s minority in the Lower House, any LDP President must be able to garner enough support from opposition parties to pass legislation, which narrows the list of suitable candidates. The JPY has softened in response to political uncertainty with USD/JPY rebounding above 148, and a JPY recovery awaits clarity on the political front. Meanwhile, the US and Japan had formalized their trade deal today, with Japan committing to invest USD550bn in the US and increasing market access for US firms, and the US setting a 15% tariff rate for nearly all Japanese imports, including autos.

USD/CNH has held in a tight range around 7.12-7.14, with RMB supported by strong sentiment in Chinese equity markets and a series of low USD/CNY fixings around 7.10 this week. Interestingly, Chinese policymakers are reportedly considering measures to cool stock market fervour, which could include the removal of short selling curbs. This may not necessarily be implemented in our view, as the current rally is occurring after a period of torpor, and the CSI300 index is still far from its 2021 highs. In any case, the Chinese equity rally is not at odds with the ongoing rally in global equity markets, with the S&P500 hitting another record high overnight.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Asset)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.