Related Insights

Following the start of Operation Epic Fury, GBP (-1.9%) was more resilient than the EUR (-2.2%) and CHF (-3.8%) in March.The UK was slightly more insulated from the global energy shock. Only about 1% of the UK’s gas supply comes from Qatar via the Strait of Hormuz. The UK relies heavily on its own North Sea production and pipelines from Norway. The EU is far more exposed, with roughly 12-13% of its LNG coming through the Strait. When Hormuz was effectively closed in February, the EU had to scramble to compete for more expensive US cargoes. As a landlocked nation, Switzerland relies on transit through the EU, with its economy vulnerable to energy shocks that hit Germany and France.

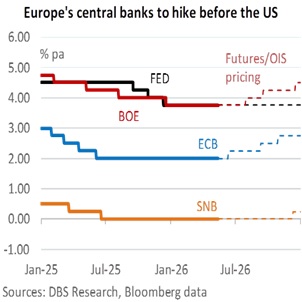

In April, GBP (+2.9%) outperformed the CHF (+2.3%) and EUR(+1.5%). The Bank of England has the same policy rate level as the 3.75% Fed Funds Rate, compared to the European Central Bank’s 2%, and the Swiss National Bank’s 0%. While not as physically vulnerable to the Iran conflict, the UK was not immune to headline inflation, which increased to 3.3% YoY in March, well above its 2% target. Not surprisingly, markets bet that Europe’s central banks would hike rates before the Fed, driven by US President Donald Trump’s expectation for his Fed Chair nominee, Kevin Warsh, to lower rates when he assumes office on May 15(tomorrow). Trump also pushed for “ceasefires” that raised hopes for a diplomatic off-ramp to the Iran conflict at his official summit with Chinese President Xi Jinping today.

However, GBP (-0.6%) underperformed the EUR (-0.2%) and CHF(-0.1%) in the first half of May. Markets now see GBP facing a reality check as focus shifts from the US-Iran conflict to 10 Downing Street. British Prime Minister Keir Starmer is facing significant internal pressure to resign following the ruling Labour Party’s heavy losses at the local elections and a subsequent wave of resignations, including junior ministers and parliamentary aides. Markets now see the BOE delaying its policy rate hike to July vs. the previous expectation of a rate hike with the ECB in June.

In the end, the GBP’s outlook remains tethered to the escalation or resolution of the Iran conflict, primarily because of how it dictates the USD’s strength. Despite lowered expectations, the market has not ruled out today’s Trump-Xi summit as a turning point for an off-ramp. Trump’s consistent preference for lower interest rates often aligns with a weaker USD to boost US exports, but the inflationary pressure from the Iran war makes it difficult for Warsh to justify aggressive rate cuts. US Treasury Secretary Scott Bessent’s visit to Japan appears to prioritize stability over competitive devaluation, as he aligns with Japan in avoiding disorderly currency volatility. History shows that domestic UK politics drives GBP when it threatens fiscal solvency in a major way, such as Lizz Truzz’s mini-budget crisis in 2022. Like it or not, GBP is still holding on to its post-Operation Epic Fury appreciation, in contrast to EUR and CHF.

Quote of the Day

“Good people do not need laws to tell them to act responsibly, while bad people will find a way around the laws.”

Plato

May 14 in history

In 1955, the Soviet Union and seven Eastern Bloc nations signed the Warsaw Pact, a mutual defence treaty formed in response to West Germany’s integration into NATO.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.