Related Insights

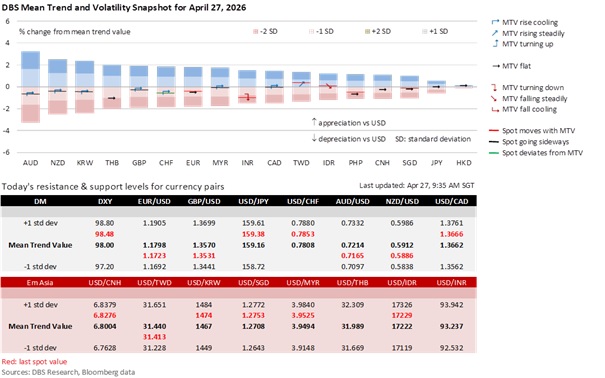

This week, currency markets face multiple cross-currents: volatile oil prices, Powell's stance on whether he will remain as Fed Governor until Jan 2028, potential rate-hike pivots at G7 central bank meetings, and the War Powers Resolution vote and deadline. The DXY Index’s rebound has stalled around 99, following its decline from 100.6 to slightly below 98 in the first half of this month.

The US Department of Justice’s (DOJ) decision on April 24 to drop its criminal probe into Fed Chair Jerome Powell has technically fulfilled Republican Senator Thom Tillis’ demand to support Kevin Warsh’s confirmation. The Senate Banking Committee should confirm Warsh as Powell’s successor at a scheduled confirmation vote on April 29 at 10:00 AM ET, hours before the FOMC’s interest rate decision. Warsh’s nomination had a dovish tilt, helping US equities hit new record highs over the past week despite Brent crude prices returning above $100 per barrel.

Powell’s final FOMC press conference as Chair will likely be dominated by the question of whether he intends to remain as Governor until January 2028. Powell has consistently maintained that he has "no intention of leaving" until the oversight process reaches a conclusion of "transparency and finality." While the DOJ technically signalled a retreat by referring the USD2.5 billion Fed HQ renovation probe to the Fed’s Office of Inspector General (OIG), in line with Powell’s request, the resolution remains fragile. By explicitly stating that it has no hesitation to restart a criminal investigation should new facts emerge from the OIG report, the DOJ has framed its decision as a partial reversal in spirit rather than a total exoneration.

The Bank of Japan, European Central Bank, and Bank of England are expected to remain on hold this week, but the market is pricing a hawkish pivot for rate hikes at their following meetings, diverging from expectations that Warsh’s confirmation would dampen the Fed’s high-for-longer USD premium.

Against this backdrop, a “hawkish hold” at the April 27-28 BOJ meeting will be important to offset the upward pressure on USD/JPY near 160. Apart from Governor Kazuo Ueda needing to pivot towards a 25-bps hike to 1% at the June meeting, Finance Minister Satsuki Katayama needs to recognize that markets are becoming desensitized to her verbal jawboning without follow-through action. Moreover, BOJ and MOF are also aware of the zero-sum game posed by the triple trap of higher oil prices, rising JGB yields, and JPY depreciation.

Additionally, Brent crude prices have risen back above $100 per barrel ahead of this week’s War Powers Resolution vote on April 29, which will determine if the Operation Epic Fury enters an unauthorized phase. The Trump administration is attempting to preserve its operational freedom before the formal 60-Day Constitutional Limit expires on May 1, with the dual blockade in the Strait of Hormuz and the stalled Pakistan-mediated US-Iran ceasefire talks. Markets are caught between fears of a prolonged war of attrition that could keep 20% of global oil supply under threat and hopes of a surprise off-ramp before President Donald Trump’s summit with President Xi Jinping in China in mid-May.

Quote of the Day

“Where words fail, music speaks.”

Hans Christian Andersen

April 27 in history

Ludwig van Beethoven composed his famous piano piece "Für Elise" in 1810.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.