Related Insights

Investors grappled with US trade uncertainty overnight. The Dow Jones and S&P 500 indices declined by 1.7% and 1%, respectively, after President Donald Trump responded with a maximum global tariff of 15% under Section 122 to the Supreme Court’s decision to strike down his use of the International Emergency Economic Powers Act (IEEPA) to unilaterally impose reciprocal tariffs. The tech-heavy Nasdaq Composite Index fell by 1.1%, driven by fears that AI could undermine white-collar AI profits. Investors fled to traditional safe havens. Gold prices surged by 2.4% to USD5277/oz, up 7.2% from a low of 4878 on February 17. The US Treasury 10Y yield fell 5.2 bps to the year’s low of 4.03%.

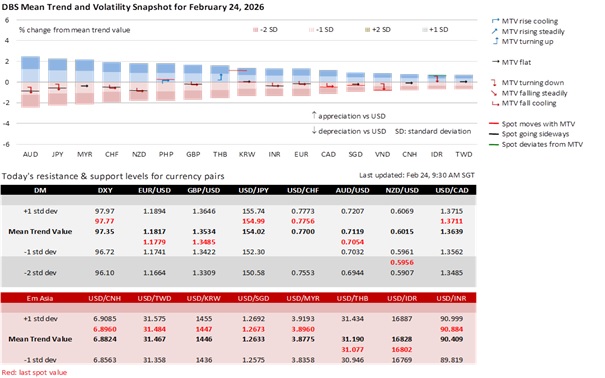

While the DXY Index was barely changed at 97.72, JPY and CHF rose by 0.26% and 0.12% respectively as havens. CAD depreciated most in the DXY market by 0.12% after Canadian officials warned that the Section 122 tariffs could leave the country worse off than before. The EU suspended the ratification of a trade deal struck in late 2025 and is seeking clarity on how the ruling impacts previous agreements. India also deferred previously scheduled talks to finalise a trade agreement due to the new legal uncertainties. EUR/USD was unchanged at 1.1785 while INR rose marginally by 0.1% to 90.88.

Fed Governor Christopher Waller did not expect the Supreme Court’s tariff ruling to affect his interest rate outlook. Waller’s decision to support a rate cut at the March 18 FOMC meeting will depend on the labour market. Today, the US Conference Board is expected to report an improvement in its consumer confidence index to 87.1 in February from 84.5 in January, driven by rises in both expectations and present situation. The market is not pricing a Fed cut at the March or April meetings because the Senate confirmation hearing of Kevin Warsh, Trump’s nominee to succeed Fed Chair Jerome Powell in mid-May, is still held up.

Focus falls on President Trump’s State of the Union Address (SOTU) on February 24 at 9:00 pm ET or February 25 at 10:00 am SGT. Trump warned that the speech would be long amid a partial government shutdown and boycotts by several House Democrats. Markets expect SOTU to become his rallying cry for the 2026 midterm elections amid sagging approval ratings. Trump is expected to address affordability issues with populist measures such as capping credit card interest rates at 10%, lowering prescription drug prices, and restricting corporate dominance of the housing market. To resell his “America First” economic vision to the public, Trump will expect Kevin Warsh to follow his roadmap toward much lower interest rates and a smaller Fed balance sheet to boost US growth to 15%.

Investors will want clarity on how Trump intends to circumvent the Supreme Court’s ruling to maintain his tariff policy, i.e., by relying on short-term emergency statutes as a bridge to establish more permanent and investigation-backed tariffs. Tariffs are Trump’s primary tools for economic and geopolitical leverage – tariff revenue to replace or offset federal income taxes, tariffs as a weapon of choice to get foreign nations into trade deals, and tariffs to force companies to move manufacturing back to the US. Foreign nations will be looking for SOTU to signal a return to constitutional norms or a more aggressive, blunt-force approach using the administration’s remaining executive powers.

In summary, the overnight price action reinforces the view that the USD is not trading purely on interest rate differential but increasingly on institutional credibility and policy coherence. The latest tariff episode adds a layer of political risk, diluting the USD’s traditional haven appeal. While it does not signal an imminent USD crisis, USD rallies could prove shallower and more episodic going forward.

Quote of the Day

"A smile is the universal welcome.”

Max Eastman

February 24 in history

Russia launched full-scale unprovoked invasion of Ukraine in 2022.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.