Related Insights

- ASEAN ADVANTAGES26 May 2025

- China’s Offset to Property Market Distress20 Mar 2025

- Optimize Your Portfolio with the Barbell Strategy25 Feb 2025

Key Points :

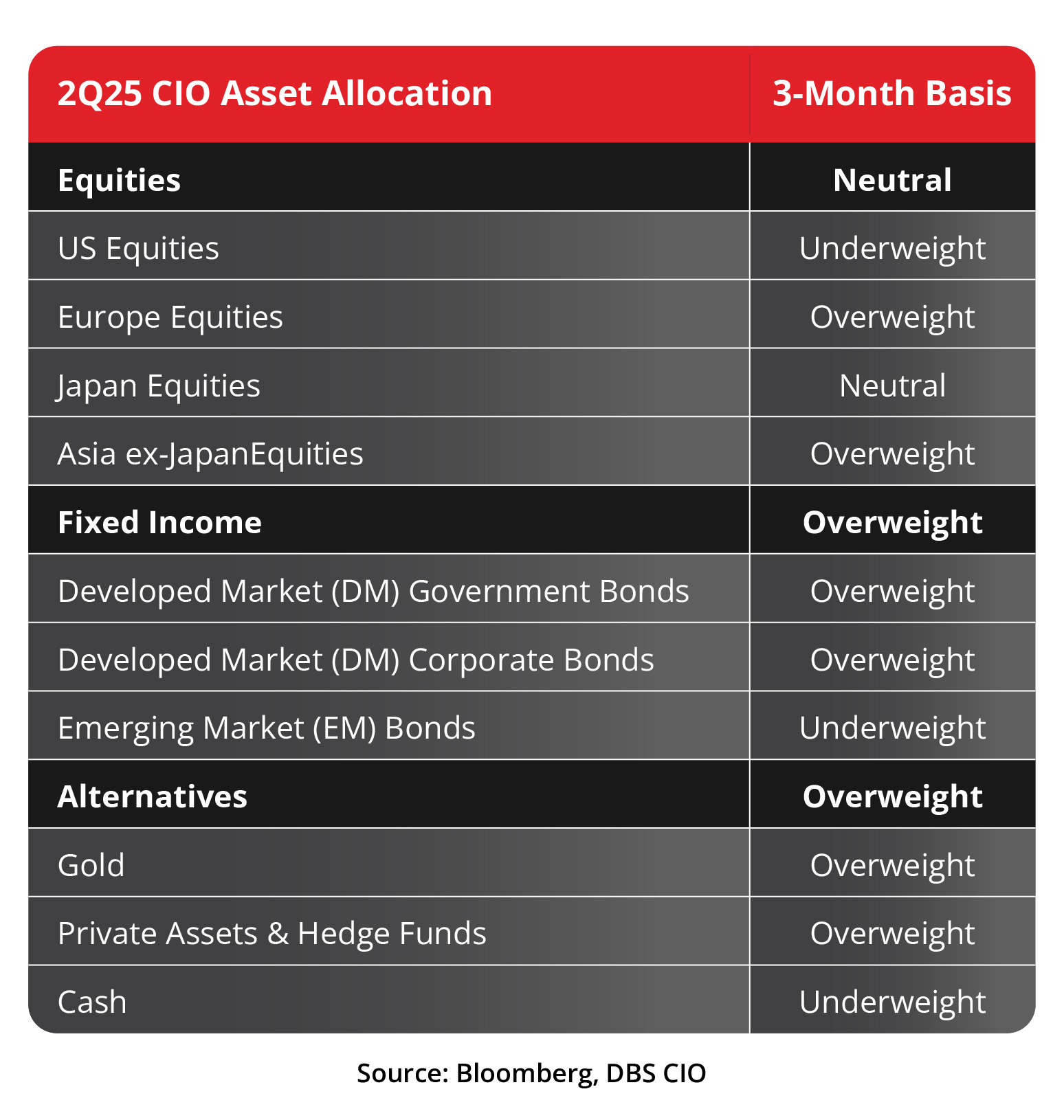

- Given shifting geopolitical winds and divergent valuations, we downgrade US equities to 3-month Underweight while upgrading Europe to 3-month Overweight.

- US equities to face near-term pain as escalation of trade tensions weighs on confidence and consumption; maintain a constructive view on US technology given long-term secular tailwinds.

- The rise of an “America First” policy will see European nations spending more on defence; Resurgent European policy stimulus, coupled with its valuation discount, provides positive tailwinds for European equities.

Navigating policy headwinds in Trump 2.0.

We have advised investors to seek opportunities beyond S&P 500 amid policy uncertainties and early signs of moderation in the US macro momentum. On the flipside, just as “US exceptionalism” is facing severe headwinds, Europe is showing strong signs of resurgence with Germany’s “whatever it takes” moment signalling the rise of policy stimulus in Germany and other parts of Europe. Given the changing geopolitics and divergent valuations between the two markets, we are making the following tactical switches for our upcoming 2Q25 CIO asset allocation:

- Downgrading US equities to 3-month Underweight while maintaining 12-month Overweight

- Upgrading European equities to 3-month Overweight while maintaining 12-month Underweight

US equities – Near-term pain on policy uncertainties; But positive view on US technology stays intact.

The initial enthusiasm surrounding fiscal easing in Trump 2.0 faded fast as the S&P 500 gave up all its post-presidential election gains. For the upcoming quarter, we advise investors to look beyond US equities given the revival of growth and policy headwinds. The escalation of trade tensions will weigh on consumer confidence and drive domestic consumption lower. The same can be said for business confidence and corporate capex. As analysts start to revise their earnings forecasts down in the coming months, it will be difficult for S&P 500 to sustain its valuation premium relative to other developed markets. On a forward P/E basis, the US trades at ca. 46% premium to developed markets (excluding US). However, despite our 3-month downgrade, we maintain a constructive view on US technology given their long-term secular tailwinds.

Europe equities – Impending rise in defence spending to drive economic and earnings growth higher. We are upgrading Europe to 3-month Overweight as shifting geopolitical winds with US adopting an “America First” policy will see European nations spending more on defence in the coming years. According to Kiel Institute, GDP growth could increase by 0.9-1.5% per year if nations :

(a) Increase defence spending to 3.5% of GDP (vs. NATO’s target of 2%) and

(b) Purchase weapons manufactured domestically in Europe. The resurgence of European policy stimulus is coming at a time when the region’s macro momentum is on the rebound and yet, the domestic equity market is trading at as discount to the rest of the developed markets.

Conclusion :

While US equities face near-term risks, technology remains a long-term growth driver. Meanwhile, European markets offer tactical upside due to fiscal stimulus and rising defence spending, creating a short-term investment opportunity.

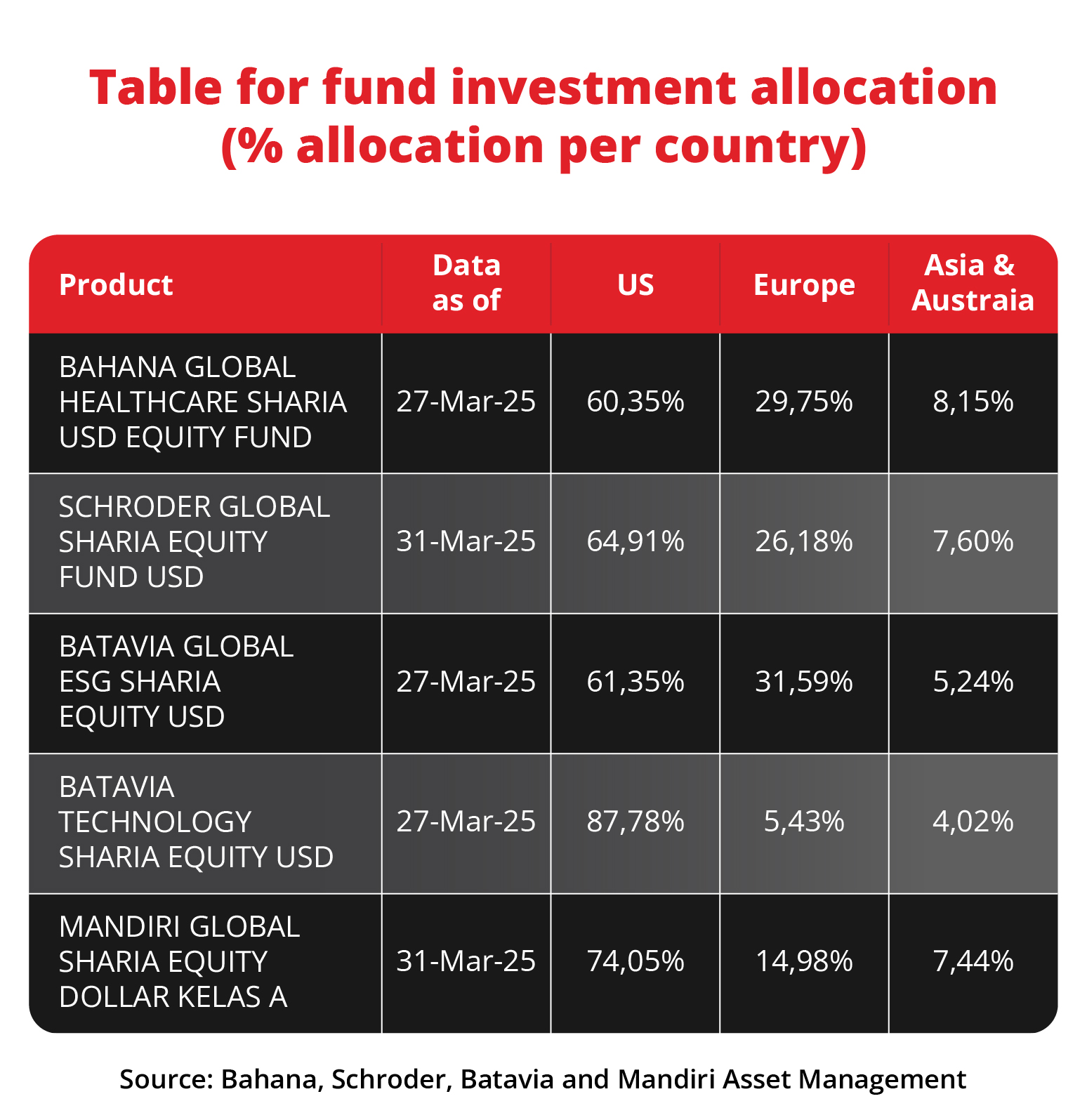

Product ideas :

Please find Offshore Sharia Funds that have allocation in US and Europe for consideration :

Ready to act now ?

Confidently make a move with curated insights and solutions for you.

Seize the opportunity on the digibank by DBS Application.

Discuss your wealth management strategy.

Find the latest insights analysed by DBS experts.

DISCLAIMER

This publication is distributed by PT Bank DBS Indonesia (DBSI). DBSI is licensed and supervised by the Indonesia Financial Services Authority (OJK). This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.

Topic

Explore more

Fund InsightsRelated Insights

- ASEAN ADVANTAGES26 May 2025

- China’s Offset to Property Market Distress20 Mar 2025

- Optimize Your Portfolio with the Barbell Strategy25 Feb 2025

Related Insights

- ASEAN ADVANTAGES26 May 2025

- China’s Offset to Property Market Distress20 Mar 2025

- Optimize Your Portfolio with the Barbell Strategy25 Feb 2025