- PE valuations are attractive again relative to public markets; timely entry point as rate cuts begin

- Returns shifting from leverage to fundamentals; greater focus on growth & operational improveme

- Primaries, co-investments, and secondaries offer complementary benefits

- Evergreen structures broaden access and resilience, especially when anchored by secondaries

Related Insights

- Gold: Looking Past the Volatility19 Feb 2026

- Global Equities: Implications of the ‘SaaS-pocalypse’16 Feb 2026

- Digital Assets: A Time to Sow, not to Reap12 Feb 2026

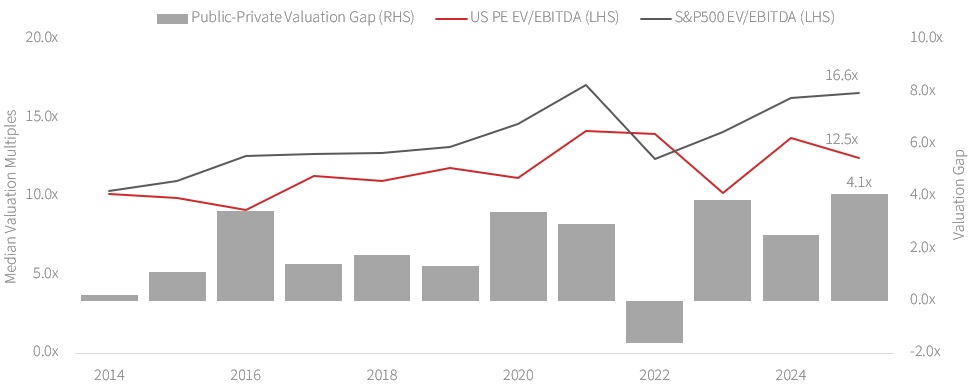

Relative value shifts back toward private markets. Private equity is undergoing a meaningful transition, and for long-term investors, this shift may be creating more attractive opportunities than we have seen in several years. To understand why, we must begin with valuations. Over the past few years, higher interest rates have slowed deal activity and moderated valuations. Meanwhile, segments of the public equity market, particularly large-capitalisation technology stocks, have appreciated sharply. The result is that private assets no longer look as relatively expensive as they once did. For investors, this creates a golden window of opportunity to capitalise on low entry multiples. Moreover, with rate cuts now set in motion, valuation multiples could see steady uplifts over time, creating a compelling case for private equity.

Less leverage, more muscle. However, valuation alone does not tell the full story. The industry itself has evolved. In an era of ultra-low interest rates, private equity managers could enhance returns by employing substantial leverage. Debt was inexpensive, and financial engineering played a significant role in amplifying gains. Today, borrowing costs are structurally higher and lenders are more selective. Consequently, managers are increasingly focused on genuine value creation by growing revenues, expanding margins, rationalising costs, streamlining operations, and deploying technology to improve productivity. Returns are becoming more closely tied to the fundamental improvement of underlying businesses rather than balance sheet leverage. From a long-term perspective, this is a promising step toward sustainable and reliable growth in private equity investments.

Planting trees to harvest for decades. For investors, access to private equity generally comes through three principal routes: primaries, co-investments, and secondaries. Primaries represent the traditional “drawdown” approach whereby capital commitments to a new vintage will only be deployed gradually over several years. Early performance often appears muted due to fees and gradual capital deployment, a dynamic known as the “J-curve.” Yet primaries provide exposure to the full life cycle of value creation. As more companies choose to remain private for longer, a significant portion of their growth occurs before any public listing. Primaries allow investors to participate in that earlier phase of expansion. Importantly, primaries remain the only viable route to access niche opportunities such as take-privates, carve-outs, and etc., which have collectively reached c.USD76bn in cumulative value.

Direct exposure with fewer tolls. Co-investments involve investing directly alongside a private equity manager into a specific company, rather than through a blind pool fund. This approach typically comes with lower fees and carried interest, which can meaningfully boost net returns. Investors also gain greater transparency and control, as capital is deployed more quickly into known assets at current market valuations. While co-investments benefit from the manager’s deal sourcing and due diligence, they are less diversified, meaning performance depends more heavily on the success of individual companies. For sophisticated investors with the resources to assess deals and the ability to tolerate concentration risk, co-investments can be an efficient way to enhance returns and manage portfolio timing, especially during periods of market uncertainty.

Second hand stakes, first order cashflows. Secondaries present yet another compelling opportunity. Here, investors purchase existing interests in private equity funds that are already partially invested. Because the underlying companies have been selected and developed to some extent, secondaries tend to mitigate the early J-curve effect and generate distributions sooner. Under certain market environments, they can also be acquired at attractive discounts, providing additional room for growth in returns. After three consecutive years of growth in secondary pricing, private equity secondaries pricing pulled back recently, availing an attractive opportunity for entry. Simultaneously, secondary market volume surged 48% y/y to a record USD240bn in 2025, setting a strong momentum for continual growth into 2026.

Evergreen by design, not by compromise. In recent years, evergreen private equity vehicles have gained massive traction, especially among individual investors. Traditional private equity structures require capital to be locked up for extended periods. Evergreen formats aim to introduce measured flexibility through periodic redemption windows, though withdrawals are typically capped and may be suspended during market stress. These vehicles often blend primaries, co-investments, and secondaries, while maintaining a sleeve of liquid assets to manage redemption needs. They represent an evolution that broadens accessibility without fundamentally altering the long-term nature of the asset class. Empirically, evergreen funds that consist predominantly of private secondaries display significantly attenuated downsides and enhanced upsides compared to drawdown funds. This underscores the synergy between the evergreen fund structure and secondaries, and the impact the blended offering can potentially deliver.

Relative value meets real growth. Taken together, the current environment marks a rare and constructive inflection point for private equity. More reasonable entry valuations, a renewed emphasis on operational value creation, and a broadened toolkit spanning primaries, co-investments, secondaries, and evergreen structures collectively enhance the risk reward profile for long term investors. As private markets mature and companies stay private for longer, these strategies offer differentiated access to growth that is increasingly less available in public markets. For investors with patience, selectivity, and a long investment horizon, private equity today is less about financial engineering and more about compounding fundamental value which may ultimately prove more resilient and rewarding over the cycle ahead.

Figure 1: Private equity valuations are at their most attractive relative to public equity in a decade

Source: Pitchbook, Bloomberg, DBS

Download the PDF to read the full report.

Topic

This information herein is published by DBS Bank Ltd. (“DBS Bank”) and is for information only. This publication is intended for DBS Bank and its subsidiaries or affiliates (collectively “DBS”) and clients to whom it has been delivered and may not be reproduced, transmitted or communicated to any other person without the prior written permission of DBS Bank.

This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.

The information herein may be incomplete or condensed and it may not include a number of terms and provisions nor does it identify or define all or any of the risks associated to any actual transaction. Any terms, conditions and opinions contained herein may have been obtained from various sources and neither DBS nor any of their respective directors or employees (collectively the “DBS Group”) make any warranty, expressed or implied, as to its accuracy or completeness and thus assume no responsibility of it. The information herein may be subject to further revision, verification and updating and DBS Group undertakes no responsibility thereof.

All figures and amounts stated are for illustration purposes only and shall not bind DBS Group. This publication does not have regard to the specific investment objectives, financial situation or particular needs of any specific person. Before entering into any transaction to purchase any product mentioned in this publication, you should take steps to ensure that you understand the transaction and has made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances. In particular, you should read all the relevant documentation pertaining to the product and may wish to seek advice from a financial or other professional adviser or make such independent investigations as you consider necessary or appropriate for such purposes. If you choose not to do so, you should consider carefully whether any product mentioned in this publication is suitable for you. DBS Group does not act as an adviser and assumes no fiduciary responsibility or liability for any consequences, financial or otherwise, arising from any arrangement or entrance into any transaction in reliance on the information contained herein. In order to build your own independent analysis of any transaction and its consequences, you should consult your own independent financial, accounting, tax, legal or other competent professional advisors as you deem appropriate to ensure that any assessment you make is suitable for you in light of your own financial, accounting, tax, and legal constraints and objectives without relying in any way on DBS Group or any position which DBS Group might have expressed in this document or orally to you in the discussion.

Any information relating to past performance, or any future forecast based on past performance or other assumptions, is not necessarily a reliable indicator of future results.

The information contained in this article has been obtained from sources believed to be reliable, but DBS makes no representation or warranty as to its adequacy, completeness, accuracy or timeliness for any particular purpose.

If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of the Information, which may arise as a result of electronic transmission. If verification is required, please request for a hard-copy version.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

If you have received this communication by email, please do not distribute or copy this email. If you believe that you have received this e-mail in error, please inform the sender or contact us immediately. DBS Group reserves the right to monitor and record electronic and telephone communications made by or to its personnel for regulatory or operational purposes. The security, accuracy and timeliness of electronic communications cannot be assured.

Please refer to the Additional Terms and Conditions Governing Digital Tokens for DBS Treasures Customers for more specific risk disclosures on trading of digital tokens.

This information does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or enter into any transaction. It does not have regard to your specific investment objectives, financial situation or particular needs. It is not intended to provide, and should not be relied upon for accounting, legal or tax advice.

Cryptocurrency trading is highly risky and prices can be very volatile. All investments come with risks and you can lose your entire investment. Before you decide to purchase an investment product, you should read all the relevant documents and carefully assess if it is suitable for you. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single asset type.

Trading in Cryptocurrencies or the instrument (“Instrument”), such as ETF, referencing or with underlying as Cryptocurrencies ("Crypto-Products”), such as Bitcoin ETFs, is highly risky and prices can be very volatile. All investments come with risks and you can lose your entire investment. By trading in Crypto-Products, you are exposed to the risks of both the Instrument and the Cryptocurrencies. Further, Crypto-Products listed on overseas exchanges may not be regulated in Singapore, and are subject to the laws and regulations of the jurisdiction it is listed in. Before you decide to buy or sell Cryptocurrencies or Crypto-Products, you should read all the relevant documents and carefully assess if it is suitable for you and/or seek advice from a financial adviser regarding its suitability. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single asset type.

To the extent permitted by law, DBS accepts no liability whatsoever for any direct, indirect or consequential losses or damages arising from or in connection with the use or reliance of this email or its contents. If this information has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses.

Please refer to Terms and Conditions governing your banking relationship with DBS for more specific risk disclosures on the Instrument (such as ETFs under Funds) and Digital Tokens.

This information is provided to you as an “Accredited Investor” (defined under the Securities and Futures Act of Singapore and the Securities and Futures (Classes of Investors) Regulations 2018) for your private use only. It is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, and may not be passed on or disclosed to any person nor copied or reproduced in any manner.

DBS (Company Registration. No. 196800306E) is an Exempt Financial Adviser as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore (the "MAS")

Related Insights

- Gold: Looking Past the Volatility19 Feb 2026

- Global Equities: Implications of the ‘SaaS-pocalypse’16 Feb 2026

- Digital Assets: A Time to Sow, not to Reap12 Feb 2026

Related Insights

- Gold: Looking Past the Volatility19 Feb 2026

- Global Equities: Implications of the ‘SaaS-pocalypse’16 Feb 2026

- Digital Assets: A Time to Sow, not to Reap12 Feb 2026