Key Points

-

Equities: ASEAN net beneficiary of higher interest rates and commodity prices; Singapore and Indonesia in sweet spots.

-

Rates: Fed Chair Powell's comments drove further flattening of the UST curve as the odds of a 50 bps move are elevated.

Equities: ASEAN’s resilience in the storm

ASEAN markets had stayed resilient in the midst of global volatility. The region returned 1% in 1Q-to-date despite global risk-off sentiments amid worries over the Federal Reserve’s tightening and Russia-Ukraine crisis. The main themes of higher interest rates benefitting the banks, higher commodity price supporting exporters, and recovery from Covid-19 will continue to support the region’s economies and equities.

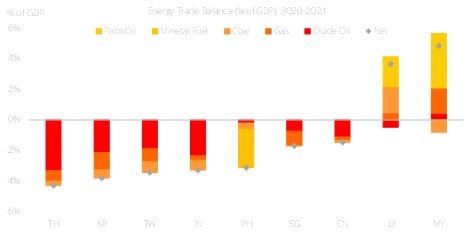

Higher commodity prices a two-edged sword for ASEAN. The region has limited exposure to Ukraine/Russia as trade dependency between the two regions are minimal, at less than 1% of total trade. However, if the crisis is prolonged, the region’s 8% trade with the European Union (EU) region could be at risk due to supply disruption and weak consumer sentiments over there.

The net impact to the region is mainly through higher commodity prices, where commodity exporting countries such as Malaysia and Indonesia should benefit with their rich palm oil, natural gas, coal, metals, and minerals resources. Thailand and Vietnam are net oil importers and should be affected by higher energy prices through deteriorating balance of payments and inflation if higher prices are left unchecked. Upstream Oil companies in Thailand, commodity producers in Malaysia and Indonesia, and shipyards in Singapore stand to benefit from higher oil prices.

Figure 1: Tailwinds for exporters, headwinds for importers

Higher Interest rates. With US Fed staying on course to deliver seven rate hikes this year on inflation worries, we could see correspondingly higher rates in ASEAN countries. However aggressive hike paths are unlikely as ASEAN have relatively contained inflation and lower external financing risks, which have given them the flexibility to stay accommodative for longer. Singapore tends to follow closely on US rate hikes and banks are the biggest beneficiaries of rate hikes on NIM expansion. The property sector could be affected negatively by higher interest rates on slower demand. However, the sector’s appeal as an inflation hedge should outweigh the burden of higher interest rates especially when interest rates are still low by historical standards. The luxury end should be more resilient. Singapore REITS as property proxies should also benefit from economy reopening while only marginally affected by higher interest rates and energy prices.

Rates: Green light for a 50 bps hike?

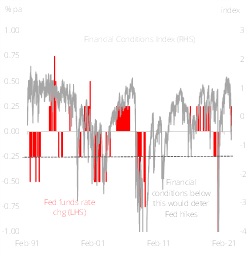

Overnight, Federal Reserve Chair Jerome Powell’s comments drove a further fear flattening in the US Treasuries curve. Specifically, the emphasis that a 50 bps move (last delivered in 2000) is on the cards led to another repricing as rate hikes get even more frontloaded. We take Powell’s comments that another hawkish shift has taken place and that the odds of a 50 bps move (perhaps even delivered back-to-back in May and June) are elevated. Our own modelled neutral Fed funds rates (using an adjusted Taylor Rule) still shows 2.75-3.00%, in line with our forecast for the upper bound at 3% in end-2023. Given inflationary prints, the Fed may want to move towards neutral as fast as reasonably possible. We had noted that financial conditions would be key. With the market becoming less focused on the Russia-Ukraine conflict and perhaps getting used to hawkish Fed rhetoric, financial conditions have continued to improve. We take that as a signal that the market is able to handle a more aggressive pace of hikes.

With the Fed singularly focused on inflation (given that the employment mandate has already been met), flat curves appear inevitable. Strategy wise, we are still wary of duration. Longer tenors embed more duration risks than shorter tenors even as the curve continues to flatten. We think that the bulk of the tightening will probably be within 21 months (by end 2023) and short tenors (out to 2Y) are likely to stay buoyant. Beyond that, we would note that the odds of a slowdown in growth/inflation would probably increase. Curve flattening could be expressed in the 2Y/5Y segment.

Our modelled neutral for 10Y yields has shifted into the 2.7-2.8% range. Current levels at 2.31% look too low in absolute terms. In relative terms, 10Y yields also look low with the curve inverted in the 3Y/10Y, 5Y,10Y segment. Taking our two models together, we forecast a flattish curve (that eventually inverts in 2023) as the Fed tightens.

Figure 1: Financial Conditions Index vs Fed