Related Insights

The Philippine central bank (BSP) is widely anticipated to deliver a third consecutive 25 bps rate cut to 5% today. BSP Governor Eli Remolona said an August cut was “quite likely” following the decline in CPI inflation to 0.9% YoY in July. With inflation below the official 2-4% target range, and fiscal flexibility limited after the mid-term elections, monetary policy is assuming a larger role in cushioning the economy from external uncertainties, such as the 19% US reciprocal tariff rate on Philippine goods. Hence, many expect BSP to provide guidance for another cut after this meeting.

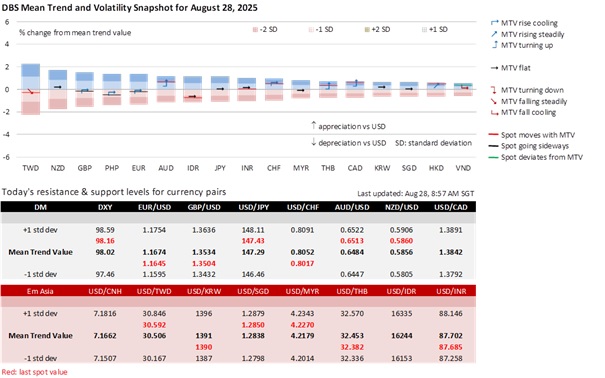

Today’s decision will unlikely weigh on the PHP, which has appreciated in August to ~57 per USD from the year’s weakest levels around 58.50. USD/PHP has been taking its cue more from the US Federal Reserve, which has signalled a rate cut in September to cushion the labour market.

The South Korean central bank (BOK) left its base rate unchanged at 2.50% for a third consecutive time. Although inflation has been stable around the official 2% target, today’s hold decision was more about maintaining financial stability. The BOK is cautious about a buoyant property market adding to the already high household debt. BOK also revised up 2025 forecast to 0.9% from 0.8% for GDP growth, and to 2% from 1.9% for CPI inflation. Real GDP growth had rebounded by 0.6% QoQ sa in 2Q25 after a 0.2% contraction in the previous quarter, posting its strongest growth since 1Q24. The KOSPI stock market has risen more than 30% YTD this year, thrice as much as the S&P 500 Index.

USD/KRW has been taking its cue from the DXY Index after Liberation Day – the day US President Trump announced US reciprocal tariffs on the world. The KRW’s appreciation in 2Q25 also stalled and corrected over the past couple of months, following the KOSPI’s rally into a consolidation. Hence, USD/KRW may revisit the year’s low around 1360 again if next month’s FOMC meeting and the coming US-China trade talks improve global risk appetite amid USD weakness again.

Quote of the Day

“Darkness cannot drive out darkness; only light can do that. Hate cannot drive out hate; only love can do that.”

Martin Luther King Jr.

August 28 in history

Martin Luther King Jr. delivered his "I Have a Dream" speech during the March on Washington in 1963.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Asset)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related Insights

Related Insights

DISCLAIMER