Related Insights

Last week ended with peak inflation as the overarching theme. US core PCE inflation did not accelerate in May, rising at the same 0.3% MoM pace as April. Markets could not brush off the back-to-back monthly declines of more than 20% in Brent crude prices to around pre-war levels. Frustrated that pump prices did not decline despite sharply lower crude prices, US President Donald Trump instructed the Department of Justice to launch an immediate investigation into major oil and refining companies for price gouging, demonstrating an unwillingness to tolerate a Fed rate hike before the November midterm elections.

The US Bureau of Labor Statistics will release the nonfarm payroll data a day earlier on Thursday, to observe Independence Day on Friday. Markets reckon that a June print of 100-130k would support a “low hire, low fire” labour market that does not rekindle a wage-price spiral or second-round effects. The ISM Price Paid sub-indices in the Manufacturing Survey on July 1 and the Services Survey on July 6 will be important previews of the June CPI report on July 14.

Hence, the European Central Bank Forum in Sintra from June 29 to July 1 provides a perfect window for central bank chiefs to adopt “vigilant neutrality.” The panel discussion on July 1 featuring ECB President Christine Lagarde, Fed Chair Kevin Warsh, Bank of England Governor Andrew Bailey, and Bank of Canada Governor Tiff Macklem will offer a sigh of cautious relief that fading oil-driven headline inflation is opening a window to stay on the sidelines without stressing domestic demand. The Eurozone June CPI estimate, also out on July 1, is expected to remain subdued at 0.1% MoM, after decelerating to 0.1% in May from 1% in April.

Given that this is Fed Chair Kevin Warsh’s international debut in Sintra, expect the panel to discuss the need to uphold central bank independence against political interference. Warsh’s push to end forward guidance at the Fed appears to restore the element of surprise of the Greenspan era. The ECB will likely stand by the need for qualitative framing that holds the Eurozone together after the sovereign debt crisis. The BOE’s new Bernanke framework aims to counter uncertainty by publishing more information, not less, to provide investors with alternative scenarios to manage risks.

The market's lack of panic over the recent military friction between the US and Iran is a direct result of diplomatic deals that have legally cleared the way for a flood of Iranian oil to re-enter global supply lines. On June 17, President Trump and Iranian President Masoud Pezeshkian signed the Memorandum of Understanding, an interim ceasefire deal explicitly structured to reopen the blockaded Strait of Hormuz. The US Treasury followed up on June 22 by issuing General License X, a sweeping 60-day sanctions waiver that allows for the outright production, sale, delivery, and offloading of Iranian-origin crude and petrochemicals through August 21.

Towards the end of the week, expect President Trump to heavily take credit for the recent physical drop in global oil prices during the 250th anniversary of American Independence and pitch himself as the populist defender of the American worker against greedy corporate middlemen. Trump will likely use the massive platform to signal his readiness to impose tariffs on international trading partners whose economic policies hurt the US manufacturing sector.

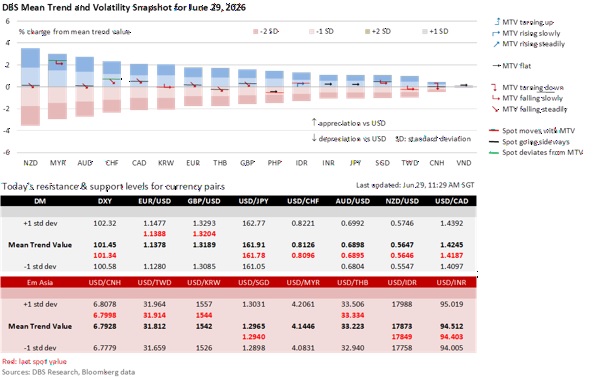

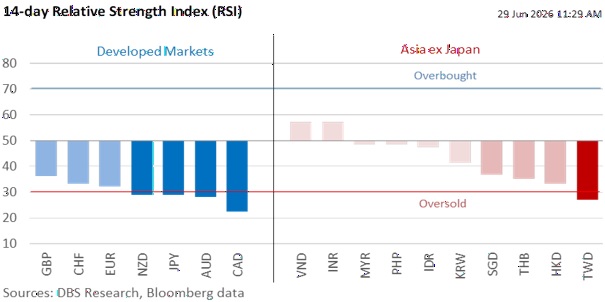

Overall, this week could be about clarification rather than tactically positioning for a new multi-month trend in the foreign exchange market.

Quote of the Day

“An iPod, a phone, an internet mobile communicator. These are NOT three separate devices! And we are calling it iPhone! Today Apple is going to reinvent the phone. And here it is.”

Steve Jobs

June 29 in history

The first version of the Apple iPhone officially went on sale to the public in 2007.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.

Related Insights

Related Insights

DISCLAIMER