Related Insights

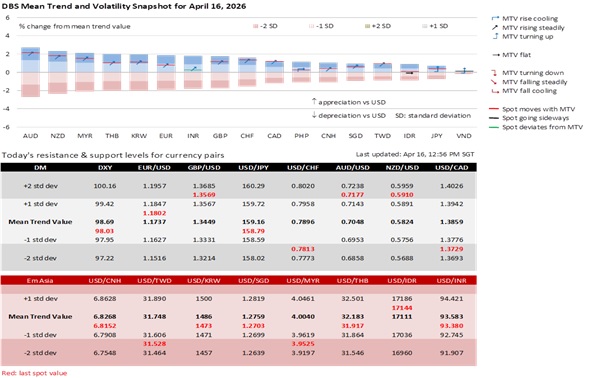

Markets are now pricing in a diplomatic resolution between US and Iran amid reports of ongoing talks, with risk assets rallying and the USD easing. The DXY index has fallen for 8 consecutive trading days towards 98 and is now at its lowest level since the outbreak of the conflict. By and large, it is fair to conclude that US/Israeli strikes have failed to achieve the strategic objective of turning Iran away from its nuclear goals, and markets are now signalling that the resumption of talks is the better path for US policymakers to pursue. China President Xi has also signalled his support for diplomacy, saying that China will continue to play a constructive role by promoting peace and dialog.

The recovery of the S&P500 to its pre-conflict level does not mean that supply chains will also fully revert to normal. Qatar’s Finance Minister Al Kuwari said that he expects the full-fledged impact beyond elevated energy prices to come in one or two months, seeing risks of energy shortages for some countries and a food crisis from a lack of fertilizers. He also said Qatar could take 5 years to restore facilities and exports damaged by the conflict. The upshot is that commodity prices are likely to be elevated on structural supply disruptions, which should support commodity exporters’ currencies, including AUD and CAD.

JPY’s recovery has trailed behind G10 peers this week, after BOJ Governor Ueda dampened hopes of an April rate hike by flagging uncertainty in the Middle East. USD/JPY is now consolidating around 159, with Japan’s Finance Minister Katayama saying yesterday that she had discussed FX issues with US Treasury Secretary Bessent, and that the authorities are prepared for bold action if needed. Markets are wary of intervention by Japan if USD/JPY tests above 160, and her rhetoric could keep JPY supported even as rate hike expectations diminish.

Quote of the Day

“If I have seen further than others, it is by standing upon the shoulders of giants.”

Isaac Newton

April 16 in history

Queen Anne of England knighted scientist Isaac Newton at Trinity College, Cambridge, in 1705.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates, Digital Assets or Commodities)[1]

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

[1] This disclaimer may not apply if the applicable assets fall within the definition of 'financial instruments' that are set out in Article 2(1) EU MAR (e.g. financial instruments that are traded on a regulated market, MTF or OTF, etc.). Section C of Annex I of MiFID2 specifies these 'financial instruments'.

Related Insights

Related Insights

DISCLAIMER