Related Insights

- USD Rates: War is inherently inflationary12 Mar 2026

- USD Rates: Inflation lurks 11 Mar 2026

- Circuit breaker hope, a China Summit pivot, and the USD’s real rate trap 11 Mar 2026

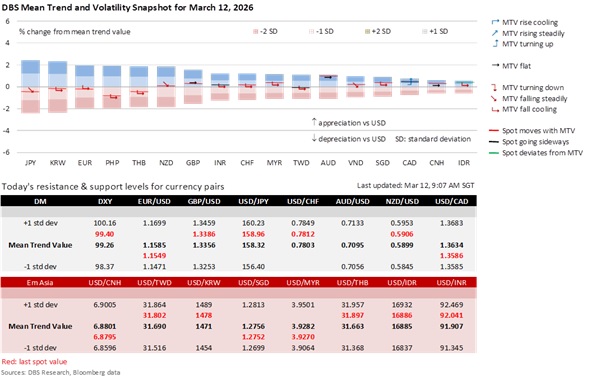

Caution is warranted with USD/JPY at the year's high after Operation Epic Fury, as the pair tests the psychologically significant 159-160 resistance zone amid a dense "geopolitical cloud." While the flight to safety and surging energy costs have favoured the USD over the JPY, the Bank of Japan is expected to deliver a hawkish hold at its March 19 meeting to maintain its path of interest rate normalization. By distinguishing between temporary supply-led inflation driven by the Strait of Hormuz chokepoint and the sustainable demand-pull inflation signalled by robust Shunto wage increases, BOJ Governor Kazuo Ueda may also be waiting for a potential diplomatic off-ramp on Iran during US President Donald Trump’s visit to China on March 31-April 2.If the Trump-Xi summit successfully de-escalates the Iran conflict and cools oil prices, the current fundamental floor for USD/JPY could give way, making any aggressive long positions at these multi-decade highs particularly vulnerable to both a shift in sentiment and the ever-present threat of Japanese Ministry of Finance intervention.

AUD has emerged as a primary outlier in the G10 space, demonstrating significant resilience against the volatility of the ongoing Iran conflict. This outperformance is driven by stark monetary policy divergence, as the Reserve Bank of Australia maintains a distinct hawkish stance relative to its peers. Following RBA Deputy Governor Andrew Hauser’s recent affirmation that inflation remains the priority of the dual mandate, noting that price pressures were already exceeding February projections prior to the Iran-related energy shock, markets have aggressively repriced the March 17 policy path. With a 66% probability now factored in for a back-to-back 25 bps hike to 4.10%, AUD/USD reclaimed the 0.7118 level held prior to Operation Epic Fury, reaching a Wednesday high of 0.7187. This price action suggested that the RBA’s commitment to curbing secondary inflationary effects from elevated energy costs is currently outweighing broader "risk-off" sentiment.

Meanwhile, the Office of the US Trade Representative (USTR) initiated a sweeping set of Section 301 investigations targeting 16 major economies, including China, the European Union, South Korea, Japan, and India, to address "structural excess capacity and production" in manufacturing. This move serves as the administration’s "Plan B" following the Supreme Court’s February 20 ruling that invalidated previous tariffs imposed under the International Emergency Economic Powers Act (IEEPA). By pivoting to Section 301, the USTR aims to establish a more durable legal basis for tariffs before the temporary Section 122 global 10% rate expires in July. While existing Section 301 actions against China remain largely suspended until November 2026, this new wave of probes signals a broadening of trade enforcement. A public docket for comments will open on March 17, with hearings scheduled for May, focusing on trade partners that maintain significant bilateral surpluses and "idle production capacity" detached from global demand. While President Trump aims to leverage the new Section 301 findings to justify extending and potentially escalating global Section 122 tariffs from 10% to 15% after the July expiry deadline, a significant fiscal reversal is still imminent. The US Customs and Border Protection has confirmed that its streamlined system for refunding previously collected IEEPA duties is scheduled to go into operation in late April.

Quote of the Day

"I slept and dreamt that life was joy. I awoke and saw that life was service. I acted and behold, service was joy.

Rabindranath Tagore

March 12 in history

The Czech Republic, Hungary, and Poland officially joined NATO in 1999, marking the first eastward expansion of the alliance to include former Warsaw Pact members.

Topic

GENERAL DISCLOSURE/ DISCLAIMER (For Macroeconomics, Currencies, Interest Rates & Digital Assets)

The information herein is published by DBS Bank Ltd and/or DBS Bank (Hong Kong) Limited (each and/or collectively, the “Company”). It is based on information obtained from sources believed to be reliable, but the Company does not make any representation or warranty, express or implied, as to its accuracy, completeness, timeliness or correctness for any particular purpose. Opinions expressed are subject to change without notice. This research is prepared for general circulation. Any recommendation contained herein does not have regard to the specific investment objectives, financial situation and the particular needs of any specific addressee. The information herein is published for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees, who should obtain separate legal or financial advice. The Company, or any of its related companies or any individuals connected with the group accepts no liability for any direct, special, indirect, consequential, incidental damages or any other loss or damages of any kind arising from any use of the information herein (including any error, omission or misstatement herein, negligent or otherwise) or further communication thereof, even if the Company or any other person has been advised of the possibility thereof. The information herein is not to be construed as an offer or a solicitation of an offer to buy or sell any securities, futures, options or other financial instruments or to provide any investment advice or services. The Company and its associates, their directors, officers and/or employees may have positions or other interests in, and may effect transactions in securities mentioned herein and may also perform or seek to perform broking, investment banking and other banking or financial services for these companies. The information herein is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of or located in any locality, state, country, or other jurisdiction (including but not limited to citizens or residents of the United States of America) where such distribution, publication, availability or use would be contrary to law or regulation. The information is not an offer to sell or the solicitation of an offer to buy any security in any jurisdiction (including but not limited to the United States of America) where such an offer or solicitation would be contrary to law or regulation.

[#for Distribution in Singapore] This report is distributed in Singapore by DBS Bank Ltd (Company Regn. No. 196800306E) which is Exempt Financial Advisers as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore. DBS Bank Ltd may distribute reports produced by its respective foreign entities, affiliates or other foreign research houses pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, DBS Bank Ltd accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact DBS Bank Ltd at 65-6878-8888 for matters arising from, or in connection with the report.

DBS Bank Ltd., 12 Marina Boulevard, Marina Bay Financial Centre Tower 3, Singapore 018982. Tel: 65-6878-8888. Company Registration No. 196800306E.

DBS Bank Ltd., Hong Kong Branch, a company incorporated in Singapore with limited liability. 18th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

DBS Bank (Hong Kong) Limited, a company incorporated in Hong Kong with limited liability. 11th Floor, The Center, 99 Queen’s Road Central, Central, Hong Kong SAR.

Virtual currencies are highly speculative digital "virtual commodities", and are not currencies. It is not a financial product approved by the Taiwan Financial Supervisory Commission, and the safeguards of the existing investor protection regime does not apply. The prices of virtual currencies may fluctuate greatly, and the investment risk is high. Before engaging in such transactions, the investor should carefully assess the risks, and seek its own independent advice.

Related Insights

- USD Rates: War is inherently inflationary12 Mar 2026

- USD Rates: Inflation lurks 11 Mar 2026

- Circuit breaker hope, a China Summit pivot, and the USD’s real rate trap 11 Mar 2026

Related Insights

- USD Rates: War is inherently inflationary12 Mar 2026

- USD Rates: Inflation lurks 11 Mar 2026

- Circuit breaker hope, a China Summit pivot, and the USD’s real rate trap 11 Mar 2026

DISCLAIMER