- Maintain cautious view on luxury due to anticipated slowdown in US, China, Japan consumer spending

- Luxury sector earnings growth revised down significantly since Liberation Day

- Favour companies with low US exposure, strong pricing power, brand desirability, robust fundamentals

- Selective opportunities on Quiet Luxury brands as they better able to weather the current climate

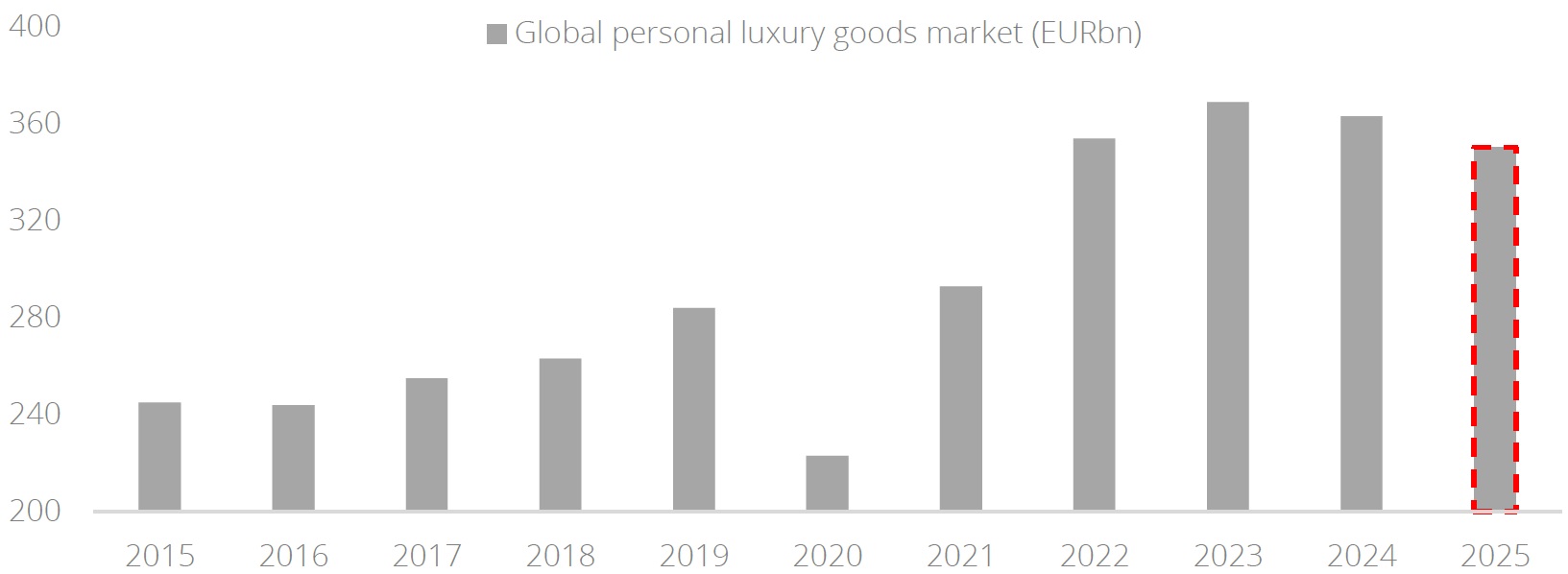

Cautious stance on weakening luxury market. A sense of caution pervades the luxury sector, with Bain & Company forecasting a contraction of 2-5% in 2025. This anticipated downturn is primarily attributed to the weakening of consumer discretionary spending across key markets, notably the US and China, as ongoing economic uncertainty weighs on consumer confidence. Even the resilient Japanese luxury market, which performed strongly in 2024, is experiencing a slowdown this year due to declining tourist spending, especially from Chinese, impacted by a strengthening yen.

15% tariffs on EU goods still pose a meaningful risk. The EU and US have agreed on 15% US tariffs on EU imports, with EU goods already facing a 10% levy since Liberation Day. While the tariffs are lower than Trump’s 30% threats earlier this month, the luxury sector is unlikely to benefit from this relief and will continue to face demand pressures amid a deteriorating global outlook. Accordingly, global luxury sector earnings growth forecast has been revised down to -3% from +12% at the start of April.

Sector-specific exemptions are unlikely due to limited manufacturing capacity within the US. Luxury brands may respond by raising prices in the US, prompting tourism to Europe. Shifting production overseas will be limited due to specialised craftmanship and skilled labour shortage. However, fully passing the increased costs to US consumers is also unlikely given the weak consumer sentiment.

Given this outlook, we favour luxury companies with i) lower exposure to the US market, ii) strong pricing power and brand desirability, allowing them to capture a structurally growing ultra-high-end demand, and iii) robust underlying fundamentals as they are better equipped to weather near-term pressures.

Quiet Luxury prevails. As highlighted on our report Luxury, Redefined, Quiet Luxury brands are better positioned to withstand the current environment given its quality excellence, strong brand heritage, and product offering exclusive to the most affluent clients. The luxury market has been experiencing shifts in consumer preferences where consumers are desiring Quiet Luxury aesthetics and exclusivity, and timeless, investment-grade jewelleries. In 2024, demand for jewellery remained robust with 2% market growth, as reported by Bain & Company, while the leather goods market weakened by 5%.

Affluent individuals continue to spend. This market’s resilience stems from the fact that high-net worth individuals’ spendings are more bolstered by economic headwinds. The most affluent clientele may only represent less than 1% of the global luxury market, but are responsible for a remarkable 23% of the total value in 2024. Boston Consulting Group indicates that 85% of these top-tier customers anticipate maintaining or increasing their spending in the near future. In contrast, a more cautious outlook prevails among aspirational customers, who comprise 60% of global luxury market. 65% expect to maintain or reduce their spending levels, reflecting a sluggish outlook for the loud luxury market.

OBBB a tailwind for Quiet Luxury. Trump's "One Big Beautiful Bill" (OBBB) has sparked market concerns about its potential to dampen US consumer spending. The Congressional Budget Office has highlighted the bill's uneven distribution of benefits, projecting that the wealthiest individuals will enjoy annual savings of 2.3%, while those with the lowest earnings could face annual losses of 3.9%. This disparity raises concerns about the bill's impact on overall consumer confidence and spending. However, we anticipate that the financial repercussions for high-net-worth individuals will be minimal, bolstering the continued demand for Quiet Luxury.

Figure 1: Luxury market is poised to see decline in 2025

Source: Bain & Company, DBS

Download the PDF to read the full report.

Topic

This information herein is published by DBS Bank Ltd. (“DBS Bank”) and is for information only. This publication is intended for DBS Bank and its subsidiaries or affiliates (collectively “DBS”) and clients to whom it has been delivered and may not be reproduced, transmitted or communicated to any other person without the prior written permission of DBS Bank.

This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.

The information herein may be incomplete or condensed and it may not include a number of terms and provisions nor does it identify or define all or any of the risks associated to any actual transaction. Any terms, conditions and opinions contained herein may have been obtained from various sources and neither DBS nor any of their respective directors or employees (collectively the “DBS Group”) make any warranty, expressed or implied, as to its accuracy or completeness and thus assume no responsibility of it. The information herein may be subject to further revision, verification and updating and DBS Group undertakes no responsibility thereof.

All figures and amounts stated are for illustration purposes only and shall not bind DBS Group. This publication does not have regard to the specific investment objectives, financial situation or particular needs of any specific person. Before entering into any transaction to purchase any product mentioned in this publication, you should take steps to ensure that you understand the transaction and has made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances. In particular, you should read all the relevant documentation pertaining to the product and may wish to seek advice from a financial or other professional adviser or make such independent investigations as you consider necessary or appropriate for such purposes. If you choose not to do so, you should consider carefully whether any product mentioned in this publication is suitable for you. DBS Group does not act as an adviser and assumes no fiduciary responsibility or liability for any consequences, financial or otherwise, arising from any arrangement or entrance into any transaction in reliance on the information contained herein. In order to build your own independent analysis of any transaction and its consequences, you should consult your own independent financial, accounting, tax, legal or other competent professional advisors as you deem appropriate to ensure that any assessment you make is suitable for you in light of your own financial, accounting, tax, and legal constraints and objectives without relying in any way on DBS Group or any position which DBS Group might have expressed in this document or orally to you in the discussion.

Any information relating to past performance, or any future forecast based on past performance or other assumptions, is not necessarily a reliable indicator of future results.

The information contained in this article has been obtained from sources believed to be reliable, but DBS makes no representation or warranty as to its adequacy, completeness, accuracy or timeliness for any particular purpose.

If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of the Information, which may arise as a result of electronic transmission. If verification is required, please request for a hard-copy version.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

If you have received this communication by email, please do not distribute or copy this email. If you believe that you have received this e-mail in error, please inform the sender or contact us immediately. DBS Group reserves the right to monitor and record electronic and telephone communications made by or to its personnel for regulatory or operational purposes. The security, accuracy and timeliness of electronic communications cannot be assured.

Please refer to the Additional Terms and Conditions Governing Digital Tokens for DBS Treasures Customers for more specific risk disclosures on trading of digital tokens.

This information does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or enter into any transaction. It does not have regard to your specific investment objectives, financial situation or particular needs. It is not intended to provide, and should not be relied upon for accounting, legal or tax advice.

Cryptocurrency trading is highly risky and prices can be very volatile. All investments come with risks and you can lose your entire investment. Before you decide to purchase an investment product, you should read all the relevant documents and carefully assess if it is suitable for you. Invest only if you understand and can monitor your investmen. Diversify your investments and avoid investing a large portion of your money in a single asset type.

Trading in Cryptocurrencies or the instrument (“Instrument”), such as ETF, referencing or with underlying as Cryptocurrencies ("Crypto-Products”), such as Bitcoin ETFs, is highly risky and prices can be very volatile. All investments come with risks and you can lose your entire investment. By trading in Crypto-Products, you are exposed to the risks of both the Instrument and the Cryptocurrencies. Further, Crypto-Products listed on overseas exchanges may not be regulated in Singapore, and are subject to the laws and regulations of the jurisdiction it is listed in. Before you decide to buy or sell Cryptocurrencies or Crypto-Products, you should read all the relevant documents and carefully assess if it is suitable for you and/or seek advice from a financial adviser regarding its suitability. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single asset type.

To the extent permitted by law, DBS accepts no liability whatsoever for any direct, indirect or consequential losses or damages arising from or in connection with the use or reliance of this email or its contents. If this information has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses.

Please refer to Terms and Conditions governing your banking relationship with DBS for more specific risk disclosures on the Instrument (such as ETFs under Funds) and Digital Tokens.

This information is provided to you as an “Accredited Investor” (defined under the Securities and Futures Act of Singapore and the Securities and Futures (Classes of Investors) Regulations 2018) for your private use only. It is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, and may not be passed on or disclosed to any person nor copied or reproduced in any manner.

DBS (Company Registration. No. 196800306E) is an Exempt Financial Adviser as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore (the "MAS")

Related Insights

DISCLAIMER