- China tech is accelerating, with strong policy support and deep engineering talent

- AI, cloud, data centres, and robotics drive rapid TAM expansion across enterprises

- Domestic substitution strengthens self-reliance as capex rises

- Innovation leadership broadens as champions and "little giants" advance monetisation

- New listings widen investment access, highlighting long-term winners in China's innovation cycle

Related Insights

- China Healthcare: From Derivative to Definitive25 Mar 2026

- US Hotels: Souring Year as Geopolitical Tensions Bite25 Mar 2026

- Gold: Near-Term Pressure24 Mar 2026

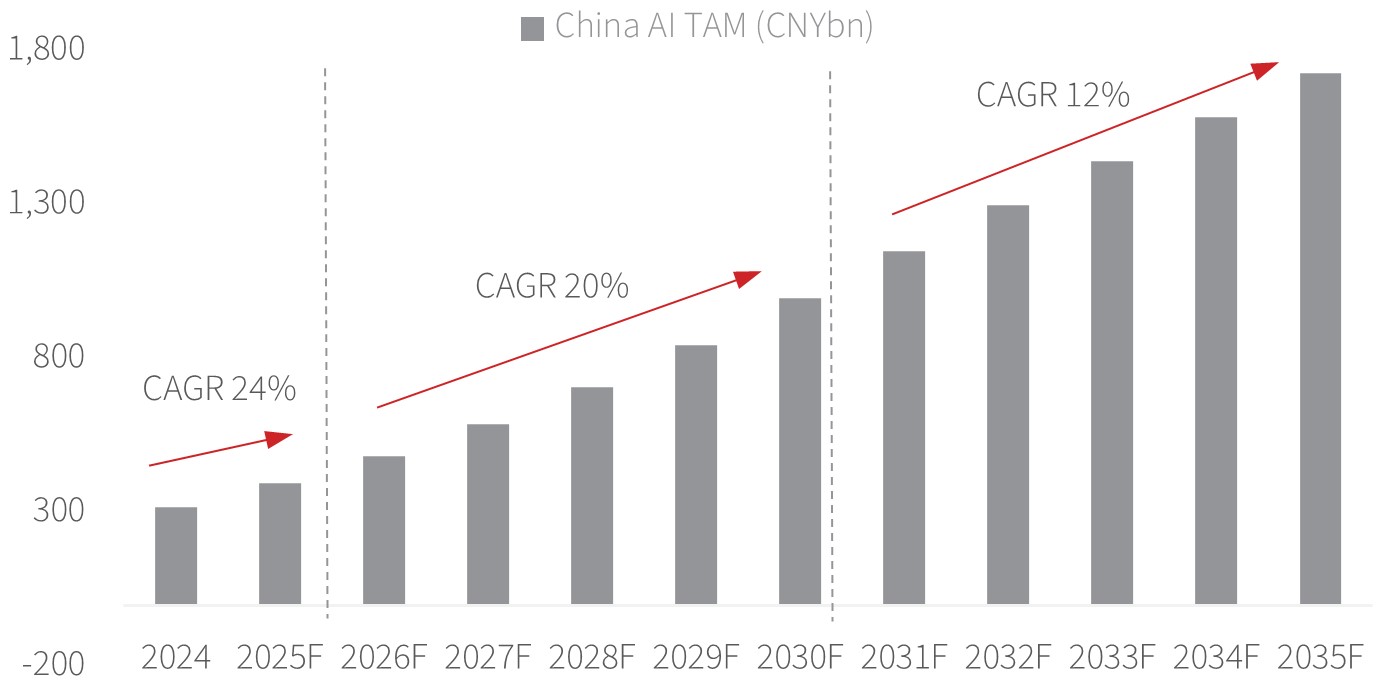

- Artificial Intelligence (AI): According to CCID Consulting (a research institute under the Ministry of Industry and Information Technology), China’s AI industry TAM is expected to reach CNY1tn in 2030 and CNY1.7tn by 2035. These are clear indications that AI will play a vital role in shaping China’s growth matrix and its path to technological ascendency.

- Cloud Computing: China’s cloud market is one of the world’s fastest-growing industry. Based on the analysis by the China Academy of Information and Communications Technology (CAICT), the TAM for cloud computing reached CNY1.1tn in 2025 and is projected to expand to CNY3.2tn by 2030 – mammoth potential by any standard. As the key foundational infrastructure of the digital economy, cloud computing remains a core pillar of China’s digital transformation journey.

- Robotics and automation: Recent advances culminated in the high‑profile, awe‑filled debut of agile humanoid robots at the Lunar New Year showcase, demonstrating sophisticated coordination, balance, and mobility through complex, synchronised performances. These acts brought to life seamless, human‑like martial‑arts movements, including precise limb articulation, coordinated sword handling, controlled backflips, and delicate physical interaction with human performers. This underscored meaningful leadership in robotic dexterity and control capabilities critical for real-world commercial deployment. The robotics and automation industries are fast emerging as cornerstones of the country’s next innovation driver. Annual industrial robot produced has surged to 773,000 units in 2025 from just 33,000 in 2015, representing a striking 37% CAGR and underscoring both scale and accelerating technological depth. This speaks volumes of domestic capabilities moving up the value chain, narrowing gaps in precision engineering, control systems, and AI-enabled automation. As global manufacturers retool for resilience, efficiency, and labour substitution, China’s integrated supply chain and policy-backed push for “smart manufacturing” position it well to capture a disproportionate share of the incremental demand, reinforcing its role as both producer and end user in the robotics ecosystem.

China has shown marked improvement in its innovation ranking through the relentless efforts by both the government and private enterprises. While gaps remain and China still trails leading countries such as the US, its Global Innovation Index (GII) score rose to 56.6 in 2025, up significantly from 46.4 at the start of last decade. This index tracks global innovation performance categories including investments, technological progress, adoption rates, and socioeconomic impact.

- Challenges: Despite rapid progress, China still relies on imports and faces technological bottlenecks in certain core areas, such as high-end semiconductor manufacturing equipment and specialty materials. In addition, Sino-US trade relationships and global geopolitical uncertainties continue to pose challenges to China’s catch-up growth.

- Opportunities: A vast domestic market, enormous R&D funding, deep engineering talent pool, and strong national support underpin sustained growth. Capital-market mechanisms such as industrial-capital linkage, the STAR Market, and the Beijing Stock Exchange facilitate financing and accelerate commercialisation. These internal advantages provide critical support for China’s path to technological advancement.

1. High-tech exports: Strengthening global standing

2. Power generation: A pillar for a future-ready economy

3. Data centres: Solidifying the digital backbone

4. Semiconductor self-sufficiency: From challenges to opportunities

Capital market returns of AI & Robotics: Fundamentals support long-term growth

Investment outlook: Focus on winners in the irreversible trend of innovation

Figure 1: China’s Artificial Intelligence market size, 2024-2035F

Source: CCID Consulting, DBS

Download the PDF to read the full report.

Topic

This information is for your private use only and may not be passed on, reposted or reproduced. The contents of this information are strictly confidential and are not transferrable, assignable or meant for reissuance to any third party, whether in whole or in part.

This information does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or to enter into any transaction. It does not have regard to your specific investment objectives, financial situation or particular needs. It is not intended to provide, and should not be relied upon for accounting, legal or tax advice.

All investments involve risks and you can lose part or all of your investment. You should carefully read the product offering documentation and any product terms before making any investment. If you have any doubt, please seek independent professional advice or otherwise you should carefully consider whether any product mentioned in this publication is suitable for you. Any investment product(s) mentioned herein is/are not the only product(s) that is/are aligned with views stated herein and may not be the most preferred or suitable product for you. There are other investment product(s) available in the market which may better suit your investment profile, objectives and financial situation.

DBS or persons/entities connected to the DBS Group may, or in the future, have interests in and may affect transactions in the underlying product(s) mentioned. Companies connected to DBS may have arrangements with the issuer(s) of the underlying product(s) to market or sell its product(s). Where any company within the DBS Group is the product provider, such company may be receiving fees from the investors. In addition, companies within the DBS Group may also perform broking, investment banking and other banking or financial services to the issuers or the related companies.

DBS Group does not make any warranty as to this information’s accuracy, timeliness, adequacy or completeness for any particular purpose, and thus accepts no responsibility for any losses whatsoever arising from or in connection with the use or reliance on this information and any related documents. Past performance is no guarantee of future results, and future results may not meet your expectations due to a variety of economic, market and other factors. This information is subject to change without notice. All figures and amounts stated are for illustration purposes only and shall not bind DBS Group.

If this information has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free.

This information is not directed to, or intended for distribution to anyone who is a citizen or resident of or located in any jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

This publication has not been reviewed or authorised by any regulatory authority in Singapore, Hong Kong, Dubai International Financial Centre, Thailand, United Kingdom or elsewhere. There is no planned schedule or frequency for updating the information discussed in this publication.

If any specific product(s) are mentioned herein, such investment product(s) is/are are not the only product(s) that is/are aligned with the views stated in the research report(s) and may not be the most preferred or suitable product for you. There are other investment product(s) available in the market which may better suit your investment profile, objectives and financial situation.

The English version of all documents shall apply and prevail over that in other languages that may be provided for your reference.

Dubai International Financial Centre

This communication is provided to you as a Professional Client or Market Counterparty as defined in the DFSA Rulebook Conduct of Business Module (the "COB Module"), and should not be relied upon or acted on by any person which does not meet the criteria to be classified as a Professional Client or Market Counterparty under the DFSA rules.

This communication is from the branch of DBS Bank Ltd operating in the Dubai International Financial Centre (the "DIFC") under the trading name "DBS Bank Ltd. (DIFC Branch)" ("DBS DIFC"), registered with the DIFC Registrar of Companies under number 156 and having its registered office at units 608 - 610, 6th Floor, Gate Precinct Building 5, PO Box 506538, DIFC, Dubai, United Arab Emirates.

DBS DIFC is regulated by the Dubai Financial Services Authority (the "DFSA") with a DFSA reference number F000164.

Where this communication contains a research report, this research report is prepared by the entity referred to therein, which may be DBS Bank Ltd or a third party, and is provided to you by DBS DIFC. The research report has not been reviewed or authorised by the DFSA. Such research report is distributed on the express understanding that, whilst the information contained within is believed to be reliable, the information has not been independently verified by DBS DIFC.

Unless otherwise indicated, this communication does not constitute an "Offer of Securities to the Public" as defined under Article 12 of the Markets Law (DIFC Law No.1 of 2012) or an "Offer of a Unit of a Fund" as defined under Article 19(2) of the Collective Investment Law (DIFC Law No.2 of 2010).

The DFSA has no responsibility for reviewing or verifying this communication or any associated documents in connection with this investment and it is not subject to any form of regulation or approval by the DFSA. Accordingly, the DFSA has not approved this communication or any other associated documents in connection with this investment nor taken any steps to verify the information set out in this communication or any associated documents, and has no responsibility for them. The DFSA has not assessed the suitability of any investments to which the communication relates and, in respect of any Islamic investments (or other investments identified to be Shari'a compliant), neither we nor the DFSA has determined whether they are Shari'a compliant in any way.

Any investments which this communication relates to may be illiquid and/or subject to restrictions on their resale. Prospective purchasers should conduct their own due diligence on any investments. If you do not understand the contents of this document you should consult an authorised financial adviser.

Hong Kong

This publication is distributed by DBS Bank (Hong Kong) Limited (CE Number: AAL664) (“DBSHK”) which is regulated by the Hong Kong Monetary Authority (the "HKMA") and the Securities and Futures Commission. In Hong Kong, DBS Private Bank is the private banking division of DBS Bank (Hong Kong) Limited.

To the extent that DBSHK does not solicit the sale of or recommend any financial product to you or where any service is provided as a transactional execution service, DBSHK is not acting as your investment adviser or in a fiduciary capacity to you. If DBSHK solicits the sale of or recommends any financial product to you, the financial product must be reasonably suitable for you having regard to your financial situation, investment experience and investment objectives. No other provision of this document or any other document DBSHK may ask you to sign and no statement DBSHK may ask you to make derogates from this clause.

In any case, DBSHK has not given and will not give any representation, guarantee or other assurance as to the outcome of any investment based on the information provided. “Financial product” means any securities, futures contracts or leveraged foreign exchange contracts as defined under the Securities and Futures Ordinance (Cap.571 of the Laws of Hong Kong). Regarding “leveraged foreign exchange contracts”, it is only applicable to those traded by persons licensed for Type 3 regulated activity. The Information has not been reviewed or authorised by the HKMA, or any regulatory authority elsewhere.

This publication is provided to you as a “Professional Investor” (defined under the Securities and Futures Ordinance of Hong Kong).

DBSHK is not the issuer of the research report unless otherwise stated therein. Such research report is distributed on the express understanding that, whilst the information contained within is believed to be reliable, the information has not been independently verified by DBSHK.

India

This document is provided by DBS Bank India Ltd. (“DBIL”) for information purpose only, on “as is” basis. It does not create any legally binding obligations on DBIL. This document is not intended to be source of advice in respect of the material presented or information published, and shall not be construed to be legal, tax, financial or investment advisory. This document is not, and should not be construed as, an offer, invitation, recommendation or solicitation to enter into any transaction in relation to any of the products and services mentioned herein. DBIL does not make any warranty of any kind, express or implied, including but not limited to warranties of completeness, accuracy of information, merchantability or fitness for a particular purpose. This document has not been registered and/or approved by any governmental or regulatory authority in any jurisdiction including but not limited to the Securities and Exchange Board of India, the Reserve Bank of India or any other governmental or regulatory body in India.

Indonesia

This publication is distributed by PT Bank DBS Indonesia (DBSI). DBSI is licensed and supervised by the Indonesia Financial Services Authority (OJK). This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such. The Customer should not rely on the information set out herein as the sole basis for any financial decision.

Singapore

This publication is distributed by DBS Bank Ltd (Company Regn. No. 196800306E) ("DBS") which is an Exempt Financial Adviser as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore (the "MAS").

This publication is provided to you as an “Accredited Investor” (defined under the Securities and Futures Act of Singapore and the Securities and Futures (Classes of Investors) Regulations 2018) or an “Institutional Investor” (defined under the Securities and Futures Act of Singapore and the Securities and Futures (Classes of Investors) Regulations 2018) for your private use only and may not be passed on or disclosed to any person nor copied or reproduced in any manner.

Thailand

This publication is distributed by DBS Vickers Securities (Thailand) Co., Ltd. (“DBSVT”).

The information contained in this publication is not intended to be either an offer, invitation or solicitation to buy or sell any securities, derivatives, or any other financial products or services, provide financial advice or investment advice, facilitate or take deposits, or provide any other financial products or financial services of any kind in any jurisdiction. This publication is provided for information purposes only and is not intended to provide, and should not be construed as, advice.

This publication has not been reviewed by any regulatory authority in Thailand and has not been registered as a prospectus with the Office of the Securities and Exchange Commission of Thailand. Accordingly, any documents and materials, in connection with the offer or sale, or invitation for subscription or purchase of the securities, derivatives, or any other financial products or services, may only be circulated or distributed by an entity as permitted by applicable laws and regulations. DBS and DBSVT does not have any intention to solicit you for any investment or subscription in the securities, derivatives, or any other financial products or services, and any such solicitation will be made by an entity permitted by applicable laws and regulations.

United Kingdom

This communication is from DBS Bank Ltd., London Branch located at 9th Floor, One London Wall, London EC2Y 5EA. DBS Bank Ltd. is regulated by the Monetary Authority of Singapore and is authorised and regulated by the Prudential Regulation Authority. DBS Bank Ltd. is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of DBS Bank Ltd., London Branch’s regulation by the Prudential Regulation Authority are available upon request.

Related Insights

- China Healthcare: From Derivative to Definitive25 Mar 2026

- US Hotels: Souring Year as Geopolitical Tensions Bite25 Mar 2026

- Gold: Near-Term Pressure24 Mar 2026

Related Insights

- China Healthcare: From Derivative to Definitive25 Mar 2026

- US Hotels: Souring Year as Geopolitical Tensions Bite25 Mar 2026

- Gold: Near-Term Pressure24 Mar 2026

DISCLAIMER