- Geopolitical tension and unilateral actions are driving an increase in global defence spending

- Defence capex carries strong upside potential, creating sustained growth opportunities in the sector

- Traditional prime defence contractors will continue to dominate

- Non-traditional high-tech disruptors are gaining traction and relevance thanks to their innovation

- Modern warfare’s swiftly shifting dynamics favours high-tech non-traditional contractors

Related Insights

- Private Equity: Relative Value Meets Real Growth20 Feb 2026

- Gold: Looking Past the Volatility19 Feb 2026

- Gold: Looking Past the Volatility19 Feb 2026

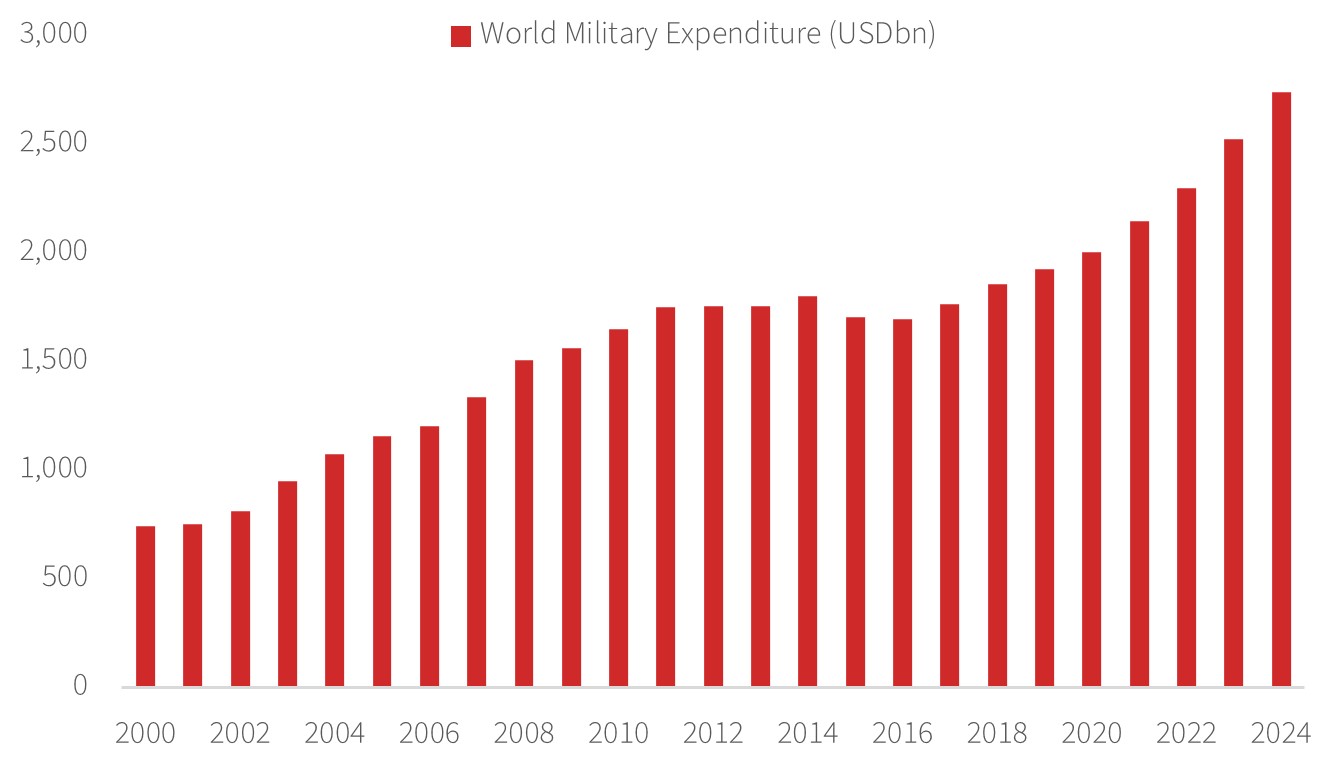

A prominent surge in defence spending. In an era where geopolitical fault lines crackle with unprecedented intensity – from Russia’s grinding assault on Ukraine to simmering American rivalries in the Western Hemisphere – the world’s governments are reaching deeper into their coffers. Global defence spending swelled to USD2.7tn in 2024 and is on track to reach >USD3.3tn by the end of the decade. This surge, propelled by NATO’s ambitious pledge to hoist expenditures to 5% of GDP by 2035 (up from a paltry 2% today), Japan’s plan to double spending by 2027, and the US’s target to raise defence spending by 50% over the same period, reflects not just paranoia but a grim calculus: the cost of deterrence in a multipolar world fraught with economic warfare, territorial spats and the spectre of great-power conflict.

The need for defence “self-sufficiency”. As the Trump administration flexes its muscles with military intervention in Venezuela, ostensibly to stabilise a region roiled by migration and oil disputes, and through eyebrow-raising overtures towards annexing Greenland for its strategic Arctic resources and rare-earth materials, the global order appears increasingly precarious. These moves, echoing 19th century gunboat diplomacy in a 21st century guise, heighten tensions by underscoring Washington’s willingness to project power unilaterally, jolting allies and adversaries alike into a scramble for defensive self-sufficiency. EU nations, wary of over-reliance on American largesse, are accelerating their push for “strategic autonomy”, while emerging powers in Asia and Latin America eye indigenous arms production to hedge against superpower whims.

The result is a stark reminder that in an age of unpredictable alliances, no country can afford to outsource its security entirely, fuelling a broader imperative for diversified supply chains and homegrown capabilities. Against this backdrop, the defence industry finds itself in a veritable golden age, albeit one laced with irony, as humanitarian appeals languish at a fraction of these sums. The beneficiaries emerge as a motley crew of incumbents and upstarts, from lumbering traditional prime contractors/enablers to nimble high-tech disruptors. Long criticised for its insularity, the industry now stands to reap rewards as global defence budgets balloon by the end of the decade, funnelling capital into everything from hypersonic missiles, defence dome, new generation fighter-jets, to AI-driven drones. With such escalations – exemplified by US’s Venezuelan foray and Greenland gambit – defence capex tilts decisively towards upside risks rather than downside revisions.

Dominance of traditional prime defence contractors. Traditional prime contractors – behemoths like Lockheed Martin, RTX, and Boeing – remain the undisputed titans, hoovering up the lion’s share of this torrent. Between 2020-24, the US “big five” alone pocketed USD771bn in Pentagon contracts, accounting nearly one-third of awarded private sector defence contracts during the period. Their edge lies in scale and incumbency: vast backlogs, proven hardware (e.g. F-35 & next-gen F-47 jets, and nuclear-powered ballistic missiles Columbia- & Virginia-class submarines), and a cosy relationship with governments prize reliability over revolution. In a spending spree, these firms thrive on “cost-plus” models where overruns are cushioned while profits, though arguably modest in margins, accrue steadily with burgeoning cashflows. As tensions escalate, for example Arctic NATO manoeuvres amid US-Danish frictions or persistent Ukraine quagmires, these traditional contractors are primed for absolute gains through continued ramp up in production for munitions and platforms. Non-US giants like the UK’s BAE Systems or Germany’s Rheinmetall mirror this trend, set to capitalise on EU’s rearmament and Asia’s export boom.

Rise of non-traditional tech disruptors. Meanwhile, a new source of intrigue is emerging in the form of non-traditional defence contractors: the agile high-tech interlopers from Silicon Valley and beyond, exemplified by Palantir’s AI analytics or Anduril’s autonomous systems. Powered by commercial tech capabilities and unburdened by legacy bureaucracies, these firms inject disruption into the sector, deploying venture-backed R&D at well over 10% of revenues (vs primes’ typical low-single digits), blistering growth rates alongside rich valuations. The Pentagon’s embrace of such “non-traditional” subcontractors open niches for innovators in drones, satellites, and robotics, where federally funded R&D boosts productivity while commercial agility yields faster and cheaper breakthroughs.

Modern warfare’s technological pivot. This evolution is accelerating with modern warfare’s inexorable march. Swarms of unmanned drones deployed with lethal efficiency in Ukraine’s trenches and Yemen’s skies herald a shift from brute-force hardware to precision, autonomy, and data dominance. AI-orchestrated systems, cyber intrusions, and hypersonic strikes demand adaptability over scale, upending dynamics: traditional primes’ grand platforms now require integrated software ecosystems, where a single drone can outperform a squadron at a fraction of the cost. This pivot favours high-tech non-traditional contractors, who leverage commercial and disruptive technology to iterate rapidly and secure more DoD (Department of Defence) contracts. That said, traditional prime contractors are also adapting through acquisitions and alliances, blending manufacturing might with startup ingenuity to expand their capabilities.

A multi-year secular growth trend. This bifurcation – stability for the old guard, velocity for the newcomers – heralds a hybrid future of partnerships and acquisitions. Risks persist: overcapacity, policy volatility, and ethical quandaries of profiting from peril. For investors, prudence dictates diversification – anchor with traditional primes for resilience, while allocating to non-traditional disruptors for tech-driven upside.

Valuation, currently at 25x and 60x average 2-year forward PE respectively for traditional and high-tech non-traditional defence contractors, is not excessively demanding when considering the industry’s prospects. As such, savvy investors should monitor and pounce on corrections, as the multi-year horizon promises enduring gains in a world where peace is increasingly a luxury. As the arms race quickens, the sector’s windfall may fortify nations while underscoring a sobering truth: in geopolitics, preparation for war often begets the very conflicts it seeks to avert.

Figure 1: Relentless global spending in defence readiness

Source: Bloomberg, DBS

Download the PDF to read the full report.

Topic

This information herein is published by DBS Bank Ltd. (“DBS Bank”) and is for information only. This publication is intended for DBS Bank and its subsidiaries or affiliates (collectively “DBS”) and clients to whom it has been delivered and may not be reproduced, transmitted or communicated to any other person without the prior written permission of DBS Bank.

This publication is not and does not constitute or form part of any offer, recommendation, invitation or solicitation to you to subscribe to or to enter into any transaction as described, nor is it calculated to invite or permit the making of offers to the public to subscribe to or enter into any transaction for cash or other consideration and should not be viewed as such.

The information herein may be incomplete or condensed and it may not include a number of terms and provisions nor does it identify or define all or any of the risks associated to any actual transaction. Any terms, conditions and opinions contained herein may have been obtained from various sources and neither DBS nor any of their respective directors or employees (collectively the “DBS Group”) make any warranty, expressed or implied, as to its accuracy or completeness and thus assume no responsibility of it. The information herein may be subject to further revision, verification and updating and DBS Group undertakes no responsibility thereof.

All figures and amounts stated are for illustration purposes only and shall not bind DBS Group. This publication does not have regard to the specific investment objectives, financial situation or particular needs of any specific person. Before entering into any transaction to purchase any product mentioned in this publication, you should take steps to ensure that you understand the transaction and has made an independent assessment of the appropriateness of the transaction in light of your own objectives and circumstances. In particular, you should read all the relevant documentation pertaining to the product and may wish to seek advice from a financial or other professional adviser or make such independent investigations as you consider necessary or appropriate for such purposes. If you choose not to do so, you should consider carefully whether any product mentioned in this publication is suitable for you. DBS Group does not act as an adviser and assumes no fiduciary responsibility or liability for any consequences, financial or otherwise, arising from any arrangement or entrance into any transaction in reliance on the information contained herein. In order to build your own independent analysis of any transaction and its consequences, you should consult your own independent financial, accounting, tax, legal or other competent professional advisors as you deem appropriate to ensure that any assessment you make is suitable for you in light of your own financial, accounting, tax, and legal constraints and objectives without relying in any way on DBS Group or any position which DBS Group might have expressed in this document or orally to you in the discussion.

Any information relating to past performance, or any future forecast based on past performance or other assumptions, is not necessarily a reliable indicator of future results.

The information contained in this article has been obtained from sources believed to be reliable, but DBS makes no representation or warranty as to its adequacy, completeness, accuracy or timeliness for any particular purpose.

If this publication has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses. The sender therefore does not accept liability for any errors or omissions in the contents of the Information, which may arise as a result of electronic transmission. If verification is required, please request for a hard-copy version.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

If you have received this communication by email, please do not distribute or copy this email. If you believe that you have received this e-mail in error, please inform the sender or contact us immediately. DBS Group reserves the right to monitor and record electronic and telephone communications made by or to its personnel for regulatory or operational purposes. The security, accuracy and timeliness of electronic communications cannot be assured.

Please refer to the Additional Terms and Conditions Governing Digital Tokens for DBS Treasures Customers for more specific risk disclosures on trading of digital tokens.

This information does not constitute or form part of any offer, recommendation, invitation or solicitation to subscribe to or enter into any transaction. It does not have regard to your specific investment objectives, financial situation or particular needs. It is not intended to provide, and should not be relied upon for accounting, legal or tax advice.

Cryptocurrency trading is highly risky and prices can be very volatile. All investments come with risks and you can lose your entire investment. Before you decide to purchase an investment product, you should read all the relevant documents and carefully assess if it is suitable for you. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single asset type.

Trading in Cryptocurrencies or the instrument (“Instrument”), such as ETF, referencing or with underlying as Cryptocurrencies ("Crypto-Products”), such as Bitcoin ETFs, is highly risky and prices can be very volatile. All investments come with risks and you can lose your entire investment. By trading in Crypto-Products, you are exposed to the risks of both the Instrument and the Cryptocurrencies. Further, Crypto-Products listed on overseas exchanges may not be regulated in Singapore, and are subject to the laws and regulations of the jurisdiction it is listed in. Before you decide to buy or sell Cryptocurrencies or Crypto-Products, you should read all the relevant documents and carefully assess if it is suitable for you and/or seek advice from a financial adviser regarding its suitability. Invest only if you understand and can monitor your investment. Diversify your investments and avoid investing a large portion of your money in a single asset type.

To the extent permitted by law, DBS accepts no liability whatsoever for any direct, indirect or consequential losses or damages arising from or in connection with the use or reliance of this email or its contents. If this information has been distributed by electronic transmission, such as e-mail, then such transmission cannot be guaranteed to be secure or error-free as information could be intercepted, corrupted, lost, destroyed, arrive late or incomplete, or contain viruses.

Please refer to Terms and Conditions governing your banking relationship with DBS for more specific risk disclosures on the Instrument (such as ETFs under Funds) and Digital Tokens.

This information is provided to you as an “Accredited Investor” (defined under the Securities and Futures Act of Singapore and the Securities and Futures (Classes of Investors) Regulations 2018) for your private use only. It is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation, and may not be passed on or disclosed to any person nor copied or reproduced in any manner.

DBS (Company Registration. No. 196800306E) is an Exempt Financial Adviser as defined in the Financial Advisers Act and regulated by the Monetary Authority of Singapore (the "MAS")

Related Insights

- Private Equity: Relative Value Meets Real Growth20 Feb 2026

- Gold: Looking Past the Volatility19 Feb 2026

- Gold: Looking Past the Volatility19 Feb 2026

Related Insights

- Private Equity: Relative Value Meets Real Growth20 Feb 2026

- Gold: Looking Past the Volatility19 Feb 2026

- Gold: Looking Past the Volatility19 Feb 2026

DISCLAIMER